How Long Does it Take to Get a Home Equity Loan?

- Published on

- 9 min read

-

Richard Haddad Managing EditorClose

Richard Haddad Managing Editor

Richard Haddad Managing EditorClose

Richard Haddad Managing EditorRichard Haddad is the managing editor of HomeLight.com. He works with an experienced content team that oversees the company’s blog featuring in-depth articles about the home buying and selling process, homeownership news, home care and design tips, and related real estate trends. Previously, he served as an editor and content producer for World Company, Gannett, and Western News & Info, where he also served as news director and director of internet operations.

At HomeLight, our vision is a world where every real estate transaction is simple, certain, and satisfying. Therefore, we promote strict editorial integrity in each of our posts.

A home equity loan can be a life-lifting tool for funding home renovations, consolidating debt, or covering unexpected expenses. But what if your financial need is pressing? How long does it take to get a home equity loan?

In this guide, we’ll provide insights and tips about home equity loans and how long it takes to access the funds you need. We’ll also share a modern way to unlock your equity so you can buy a new house before you sell your current home.

How Much Is Your Home Worth Now?

Home values have rapidly increased in recent years. How much is your current home worth now? Get a ballpark estimate from HomeLight’s free Home Value Estimator.

What is a home equity loan?

A home equity loan is a type of secured loan where your home serves as collateral. It allows homeowners to borrow against the equity they’ve built up in their property. Essentially, the loan amount is determined based on the difference between your home’s current market value and the remaining balance on your mortgage.

Home equity loans typically come with a fixed interest rate, meaning your monthly payments remain consistent throughout the loan term. This makes it easier to budget and plan your finances.

Home equity loan vs. home equity line of credit

- Home equity loan: Provides a lump sum of cash with a fixed interest rate. Monthly payments are consistent.

- Home equity line of credit (HELOC): Offers a revolving credit line, similar to a credit card, with variable interest rates. You can borrow as needed, up to a predetermined limit, and payments vary based on how much you borrow.

What are home equity loans used for?

Home equity loans are versatile and can be used for a variety of financial needs. Common uses include:

- Home improvements: Invest in significant renovations that can increase your home’s value.

- Debt consolidation: Combine multiple debts into a single payment, potentially lowering your overall interest rate and making payments more manageable.

- Major expenses: Cover costs like college tuition, medical bills, or other large expenses with the predictable repayment terms of a home equity loan.

- Key purchase or investment: The money can be used to buy a car or RV, pay for a wedding or vacation, start a business, or fund an investment.

How long does it take to get a home equity loan?

The timeline for obtaining a home equity loan can vary, typically ranging from two to six weeks. This speed of the process depends on several factors, including the lender’s efficiency, the completeness of your application, and how quickly you can supply necessary documents.

Here’s a rough breakdown of what happens during this time:

- Application and documentation: You’ll start by submitting a loan application along with required financial documents, which might include recent pay stubs, tax returns, and proof of homeownership.

- Appraisal and valuation: Most lenders require an appraisal to determine your home’s current market value, which affects the amount you can borrow.

- Underwriting and approval: Your application will go through an underwriting process where lenders assess your financial details and the appraisal report.

- Closing: Once approved, you’ll sign the final documents, and the loan will close, releasing the funds to you.

What’s required to get a home equity loan?

Securing a home equity loan requires meeting specific lender criteria to ensure you have sufficient equity and can repay the loan. Key requirements include:

- Percentage of equity in your home: Typically, you need at least 15%–20% equity in your home to qualify.

- Credit score: A higher credit score can improve your chances of approval and secure better interest rates. Most lenders look for scores above 620.

- Debt-to-income ratio (DTI): Lenders usually require a DTI ratio below 50%, with a preferred target of below 43%. This ratio helps lenders evaluate if you can handle additional debt.

- Income history: A steady income history reassures lenders that you have the means to meet monthly payments.

- Home appraisal: An appraisal is usually necessary to confirm your home’s current value and the equity available for borrowing. However, some lenders may offer options that don’t involve a full appraisal.

How much does a home equity loan cost?

The cost of a home equity loan is not just about the interest you pay but also includes closing cost fees, which generally range from 2% to 6% of the loan amount.

For example, if you take out a home equity loan of $75,000, you can expect to pay between $1,500 and $4,500 in closing costs. Here is a list of the fees that can be included in your closing costs:

- Origination fee

- Credit report fee

- Appraisal fee

- Document preparation fee

- Title search fee

- Title insurance policy

- Notary fee

- Attorney fee (in states where required)

You’ll also want to check your loan agreement for additional costs, such as annual fees for maintaining the loan or early repayment penalties that some lenders charge to offset their loss of expected interest income.

Example home equity loan payments

| Loan term | Loan amount | Interest rate | Monthly payment |

| 30-year | $75,000 | 9.15% | $611.58 |

| 20-year | $75,000 | 9.10% | $679.63 |

| 15-year | $75,000 | 9.10% | $765.17 |

| 10-year | $75,000 | 9.10% | $954.13 |

| 5-year | $75,000 | 9.10% | $1,560.52 |

Source: U.S. Bank home equity loan calculator (As of May 2024 with a 730 credit score)

When choosing which term length is best for you, consider your monthly budget. As you can see in the table above, a shorter-term loan can have a lower interest rate. The rate you pay will depend on your credit score, loan length, and the lender. It’s wise to shop around and compare interest rates.

Start Making Offers Without Waiting to Sell Your Home

Through our Buy Before You Sell program, HomeLight can help you unlock a portion of your equity upfront to put toward your next home. You can then make a strong offer on your next home with no home sale contingency.

Are there drawbacks to home equity loans?

While home equity loans can provide significant financial resources, they come with some potential drawbacks:

- Fixed loan amount: Unlike a HELOC, a home equity loan offers a lump sum, which means you can’t borrow additional funds without a new loan.

- Closing costs and fees: Home equity loans often involve closing costs and fees, which can add up to 2%-6% of the loan amount.

- Impact on future finances: Taking out a home equity loan reduces the equity you have in your home, which could impact your financial flexibility in the future.

- Risk of foreclosure: Since your home serves as collateral, failure to make payments can lead to foreclosure.

Alternatives to home equity loans

If a home equity loan doesn’t fit your financial goals or if you’re looking for different borrowing options, consider these alternatives:

- Home equity line of credit (HELOC): Unlike a home equity loan, a HELOC offers a revolving credit line to borrow from as needed, with variable interest rates.

- Personal loans: If you prefer not to use your home as collateral, a personal loan might be a suitable option. These loans often come with higher interest rates but less risk of losing your home.

- Cash-out refinance: This involves refinancing your current mortgage for more than you owe and taking the difference in cash. It can be a good choice if you can secure a lower interest rate than what you currently have.

- Credit cards: For smaller or short-term financing needs, credit cards could be a feasible alternative, especially if you can take advantage of promotional zero-interest offers.

- Retirement plan loan: Some retirement plans, such as a 401 (k), allow you to borrow from your retirement savings. The loan amount may be limited to a percentage of your vested balance or a capped amount.

- Government loans: Some government programs can provide financial assistance for home repairs and improvements, potentially offering more favorable terms than traditional home equity loans.

Can’t make additional monthly payments? Some companies offer home equity investment (HEI) programs, in which the business provides you with a lump sum of cash in exchange for a percentage of your home’s future value. An HEI is not a traditional loan, as there are no monthly payments or interest rates. Instead, when you sell your house or at the end of the contract term, the company receives a share of your property’s appreciated value along with the original investment.

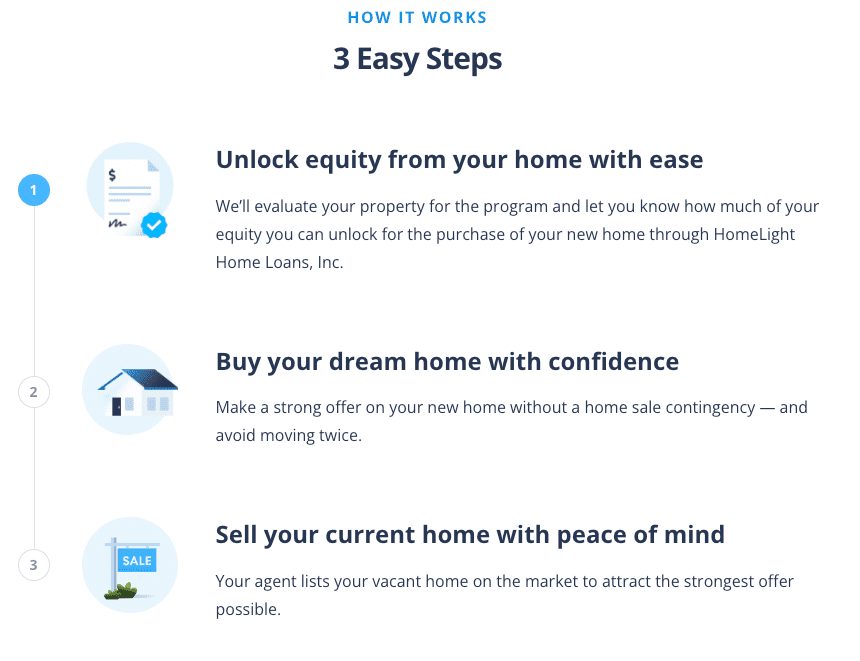

How to unlock home equity to buy before you sell

If you are a homeowner considering equity financing to purchase a new home in order to sidestep the buy-sell timing conundrum, there is a modern way to buy before you sell.

HomeLight’s Buy Before Your Sell program makes it easy to use the equity from your current home to make a strong, less contingent offer on a new home. Our innovative program, with its near-instant Equity Unlock Calculator, lets you streamline and simplify the entire buying and selling process.

Here’s how HomeLight Buy Before You Sell works:

If your home qualifies, you can get your equity unlock amount approved in 24 hours or less. No cost or commitment is required. Once approved, you can buy your next home with confidence and then sell your current home with peace of mind.

»Learn more: How to ‘Buy Before You Sell’ with HomeLight

FAQs on home equity loans

A credit score of at least 620 is typically required, but higher scores can secure better interest rates and terms.

Home equity loans are repaid in fixed monthly payments covering both principal and interest, similar to a conventional mortgage.

Yes, you can usually pay off your loan early, but check for any prepayment penalties that may apply.

It depends on your financial situation. Refinancing might be better if you can secure a lower overall interest rate than your current mortgage and home equity loan rates.

Getting a HELOC can take anywhere from two to six weeks, similar to a home equity loan, depending on various approval factors. However, some lenders expedite the process and advertise that they can provide funding in as few as five days.

Is a home equity loan right for me?

Determining whether a home equity loan is right for you depends on your financial situation. The key is to consider the costs involved, your long-term financial plans, and how comfortably you can manage the additional debt without risking your home.

If you’re considering a home equity loan to purchase a second property, HomeLight can connect you with a top real estate agent in your market who can provide expert guidance and insights.

If you’re a homeowner looking to leverage your home’s equity to avoid the risks of selling under pressure, HomeLight’s Buy Before You Sell program might be the right solution, offering a smooth, streamlined transition to your next home.

Header Image Source: (Elenaferns-photo / Depositphotos)