If you're looking to buy a house, you might be wondering if it's a good time to buy a house or if should you wait. This is a question that many people are asking themselves these days, as the housing market continues to be in flux. There is no easy answer, as it depends on a number of factors, including your individual financial situation, your long-term goals, and your local market conditions.

Is 2024 a Good Time to Buy a House?

According to the latest insights from the Fannie Mae Home Purchase Sentiment Index® (HPSI), sentiments regarding homebuying and selling conditions exhibit a mix of optimism and caution.

Current Market Sentiment

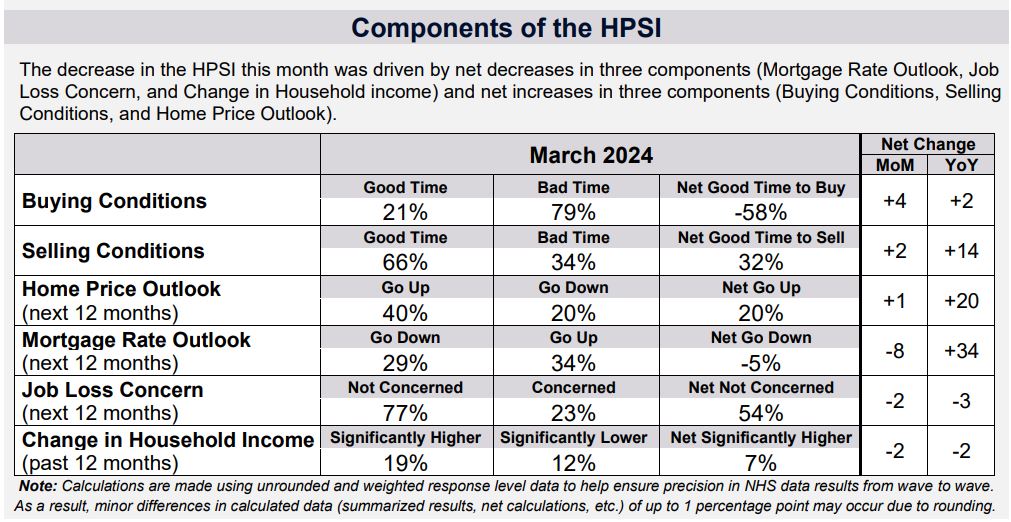

The HPSI, a key metric gauging consumer attitudes towards the housing market, saw a marginal decline of 0.9 points in March, resting at 71.9. This dip is attributed primarily to growing pessimism concerning mortgage rates, with 34 percent of consumers anticipating an upward trajectory in rates over the next year.

Despite this concern, perceptions of both homebuying and home-selling conditions experienced slight upticks in March, maintaining a trend observed over several months. However, the overarching issue of housing affordability remains a significant factor influencing consumer confidence, with only 21 percent of respondents deeming it a “good time to buy” a home.

Insights from the Experts

Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae, offers valuable insights into the shifting dynamics of the housing market. He notes that while consumer expectations may be adjusting to accommodate higher mortgage rates and home prices, the lingering impact of last year's rate surge still weighs heavily on sentiment.

Despite these challenges, Duncan remains cautiously optimistic about the market's trajectory. He anticipates a gradual increase in home listings and sales transactions in the coming year, driven not only by rate-related adjustments but also by households undergoing life changes necessitating a move.

Component Highlights

Delving deeper into the HPSI components provides a nuanced understanding of current market sentiment:

- Good/Bad Time to Buy: The proportion of respondents considering it a good time to buy a home increased slightly to 21%, accompanied by a corresponding decrease in those perceiving it as a bad time to buy.

- Good/Bad Time to Sell: Favorable sentiments towards selling a home also saw a modest rise, with 66% of respondents viewing it as a good time to sell.

- Home Price Expectations: While fewer respondents anticipate an increase in home prices over the next year, the net share still leans towards a positive outlook.

- Mortgage Rate Expectations: Concerns regarding mortgage rates are on the rise, with a notable shift towards expectations of an upward trend.

Read the full research report for additional information.

ALSO READ: When is the Best Time to Buy a House?

ALSO READ: Will the Housing Market Crash?

Should I Buy a House Now or Wait Until 2025?

The decision to buy a house is a significant step that involves a thorough assessment of your financial situation, market conditions, and personal goals. As you contemplate this important choice, it's crucial to consider both the current housing landscape and your individual circumstances.

Assessing Current Market Conditions

Understanding the current state of the housing market is essential when making a decision about buying a house. Here are some key factors to consider:

1. Interest Rates:

Mortgage interest rates play a significant role in determining the affordability of a home purchase. As of now, it's important to research and monitor interest rate trends. Low-interest rates can make homeownership more affordable, while higher rates can increase your monthly payments.

2. Home Prices:

Examine the trend of home prices in the area you're interested in. Are prices currently high or stable? Are they expected to increase or decrease in the near future? Understanding price trends can help you make an informed decision about timing your purchase.

3. Inventory Levels:

Consider the availability of homes on the market. A low inventory of homes for sale might lead to more competition among buyers and potentially higher prices. Conversely, a higher inventory might give you more options to choose from.

4. Economic Conditions:

Evaluate the broader economic environment. Factors like job stability, local job market trends, and overall economic indicators can impact your ability to make mortgage payments in the long run.

Your Personal Financial Situation

Beyond market conditions, your personal financial situation plays a crucial role in determining whether it's the right time for you to buy a house:

1. Financial Readiness:

Assess your financial health. Do you have a stable income and a good credit score? Have you saved enough for a down payment, closing costs, and potential emergencies?

2. Long-Term Goals:

Consider your long-term goals. How does buying a house fit into your overall financial plan? Are you planning to stay in the area for an extended period? Your answers can help you determine whether homeownership aligns with your life plans.

3. Budget and Affordability:

Create a detailed budget to understand how much you can comfortably afford for a monthly mortgage payment. Remember that owning a home involves more than just the mortgage; property taxes, insurance, maintenance, and utilities are additional costs to consider.

Buy a House Now or Wait?

After evaluating market conditions and your personal financial situation, you'll be better equipped to decide whether to buy a house now or wait:

Buy Now If:

- Interest rates are low, making homeownership more affordable.

- You've saved for a down payment and other associated costs.

- The housing market in your area is stable or showing positive growth.

- You've evaluated your long-term goals and buying aligns with them.

Wait If:

- Interest rates are high, and you anticipate they might decrease in the near future.

- Your financial situation needs improvement, such as increasing your credit score or saving more for a down payment.

- The housing market in your area is volatile or experiencing a downward trend in prices.

- Your long-term plans are uncertain, and committing to homeownership doesn't currently make sense.

Is it a Good Time to Buy a House for First-Time Buyers?

For first-time homebuyers, assessing whether it's a good time to purchase a house is a crucial decision. Several factors influence this decision, including mortgage credit availability, market conditions, and personal financial stability.

Mortgage Credit Availability On the Rise

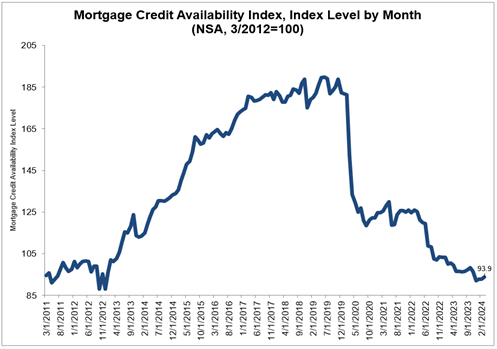

According to the Mortgage Credit Availability Index (MCAI), compiled by the Mortgage Bankers Association (MBA) using data from ICE Mortgage Technology, mortgage credit availability experienced a notable increase in March.

The MCAI, a benchmarked index set at 100 in March 2012, saw a 1.1 percent rise to 93.9 in March of this year. This uptick suggests a loosening of credit standards, a trend that can potentially benefit prospective buyers. Specifically, the Conventional MCAI increased by 2.1 percent, driven by expanded offerings in cash-out refinance loan programs across various loan types and occupancy categories.

Joel Kan, MBA's Vice President and Deputy Chief Economist, noted, “Credit availability increased in March, driven by growth in conventional credit. There were increased offerings of cash-out refinance loan programs across fixed rate and ARM loans, as well as for all occupancy types.” This expansion in credit availability marks the third consecutive month of growth, albeit still lingering around 7 percent below levels seen a year ago and closely mirroring 2012 lows.

Implications for First-Time Buyers

For first-time buyers, the surge in mortgage credit availability may present an opportune moment to enter the housing market. With lending standards showing signs of relaxation, individuals seeking to secure their first home may find more favorable conditions.

Particularly noteworthy is the growth in the Jumbo MCAI, which increased by 2.6 percent, surpassing levels seen a year ago. This increase, fueled by both non-QM and super conforming loan programs, indicates a broader spectrum of financing options available to buyers, including those eyeing higher-priced properties.

While it is advisable for prospective buyers to conduct meticulous research and consider their individual financial circumstances, the recent uptick in mortgage credit availability could signal a favorable window for first-time buyers to explore their homeownership dreams.

On the other hand:

Decreased competition: The overall housing market has shown signs of cooling down in recent months. This translates to potentially less competition for available homes, which could benefit first-time buyers.

Potentially lower mortgage rates: Experts predict a slight decrease in mortgage rates in 2024. Lower rates can translate to lower monthly payments and potentially more buying power for first-time buyers.

The decision of whether it's a good time for first-time buyers to buy a house depends on a multitude of factors beyond just mortgage credit availability. Other important considerations include:

- Personal Financial Situation: First-time buyers should assess their own financial stability, income, credit score, and existing debt. These factors play a significant role in their ability to secure a mortgage and afford homeownership.

- Real Estate Market Conditions: Housing market conditions, including supply and demand, local property values, and trends in the area, will impact whether it's a favorable time to buy. A buyer's market with more inventory and lower prices might be more appealing.

- Interest Rates: While the information provided mentioned higher mortgage rates, the actual rates prevailing in the market at the time of purchase will greatly influence the affordability of a home loan.

- Long-Term Plans: First-time buyers should consider their long-term plans. If they plan to stay in the home for several years, changes in the mortgage market might have less of an impact.

- Down Payment and Affordability: The ability to make a substantial down payment and afford monthly mortgage payments is crucial. A higher down payment can mitigate some challenges posed by tighter lending standards.

- Employment Stability: A steady job or income source is important for mortgage approval and overall financial security.

- Government Programs: Government-backed programs such as FHA loans might offer more lenient requirements for first-time buyers, making homeownership more accessible even during periods of tighter lending.

Sources:

- https://www.fanniemae.com/research-and-insights/surveys-indices/national-housing-survey

- https://www.realtor.com/research/december-2022-data/

- https://www.bankrate.com/mortgages/todays-rates/

- https://www.nar.realtor/research-and-statistics/housing-statistics/existing-home-sales

- https://www.bankrate.com/mortgages/rate-trends/

- https://www.mba.org/news-and-research/research-and-economics/single-family-research/mortgage-credit-availability-index-x241340