Real Estate Marketing & Beyond

Ask Brian is a weekly column by Real Estate Expert Brian Kline. If you have questions on real estate investing, DIY, home buying/selling, or other housing inquiries please email your questions to [email protected].

Question from Dan: Hello Brian. It’s obvious to me that paying off your home as fast as possible is good in many ways. It gives you a sense of security knowing that you’ll always have a roof over your head. By paying off a mortgage in 15 years instead of 30, it means you’ll have more money to spend on other things much sooner. In fact, it seems to me that it makes great sense to take out a 15-year mortgage and make extra payments on top of that every month. If you make an extra mortgage payment every month, you could have the mortgage paid off in less than 8 years. I’m a professional structural engineer and the math for a 15-year mortgage seems clear to me. I’m about to buy my first house and I know that almost everyone goes with a 30-year mortgage. There must be something that I’m overlooking. Why don’t most people just choose a 15-year mortgage?

Answer: Hello Dan. Your engineering background is clearly showing. From a pure math point of view, you are correct. However, most people must consider many other variables when deciding how long to finance their homes. For most people, it is a social-economic balancing equation. They must make decisions between how much they can afford to spend on a home compared to how much they have remaining to spend on the lifestyle they want.

Dan, I have a decent engineering background from my time with Boeing Aircraft company, so I appreciate how you boil it down to the simplest equation possible. However, the number of variables that most people are considering is almost endless. Just a few key variables are family size, the type of car they want to drive, the neighborhood they want to live in, the number of hours they want to work, if they want an occasional vacation, and on and on and on...

The mortgage bankers have broken this down into the simplest social-economic equation possible. It’s the debt-to-income ratio. It factors in the endless list of variables to determine how large of a mortgage they qualify for. It turns out that the lowest common denominator tends to be a 30-year mortgage. But that does not mean there are not a lot of other options for paying off a mortgage faster.

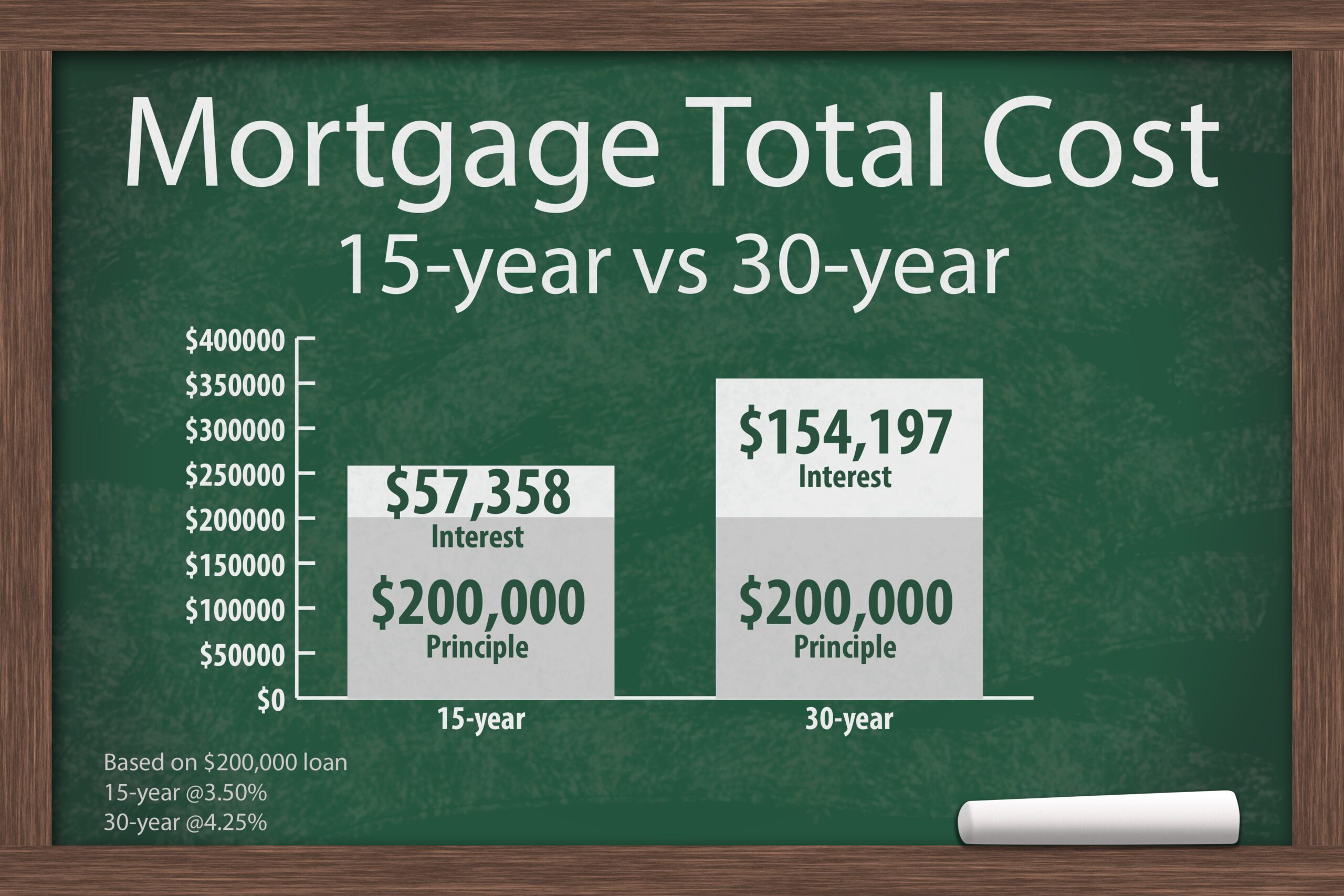

First, let’s look at some of the basic math. A $300,000 mortgage at 4.5% for 30 years will have a $1,520 monthly payment (not including taxes and insurance). At the end of 30 years, a total of $547,218 will have been paid. In comparison, the same mortgage for 15 years at 4.0% (interest rate will be lower) has a $2,219 monthly payment and a total cost of $399,432. Obviously, the 15-year mortgage saves a substantial amount of interest payments and pays the home off in half the time. But the social-economic cost is an additional $699 each month. That’s enough for a car payment and probably also enough to fund a child’s college education. That is the social-economic trade that many people choose to make. And yes Dan, you could pay the mortgage off faster by making extra payments on a 15-year mortgage, but the social-economic cost becomes even higher.

Fortunately, there are many other ways to reduce both how much a person ultimately pays for the mortgage and how long it takes to pay it off. These are choices that I think people should give more thought to. For instance, most people start earning more money as their careers advance. Their debt-to-income ratio improves. Even if the only way they could qualify for a first home is with a 30-year mortgage, after maybe 5 years, they can requalify for a 15-year mortgage. That would significantly cut down the total cost for interest and they would own the home free and clear in 20 years. Maybe in a few more years, they could start making extra payments towards the principal to reduce the total interest cost further and pay it off in less than 20 years. But there are less aggressive ways to do this.

In fact, at any time that you want, you can make additional principal payments. You don’t need a special agreement with the lender or anything. Just send in extra money each month or when you get a bonus from work or an income tax return. For instance, paying an extra $200 every month from the very start of the example $300,000 mortgage for 30 years will save $59,435 of interest costs and shorten the time to pay off the mortgage by 6 years and 4 months. People should play around with a mortgage calculator to learn what their potential savings can be in different scenarios.

There are still more ways to reduce the total cost for interest and become free and clear sooner. One is making biweekly payments. Most people get a paycheck every two weeks. You can pay half the mortgage payment from each paycheck. That reduces the principal that interest is calculated on a little sooner than waiting until the end of the month. You also end up making an extra payment each year. It doesn’t add up to a whole lot, but it is an easy way to make extra payments that do add up over 30 years.

Now probably isn’t the time to refinance because interest rates are going up but there are times when refinancing into a lower interest rate will save money. That is also a good time to consider refinancing into a 20- or 15- or 10-year mortgage instead of a new 30-year mortgage.

Dan, if you can afford to, making extra payments on a 15-year mortgage is one of the most cost-effective ways to buy a house. But along that line of thinking, paying all cash would mean not paying any interest at all and owning the home free and clear beginning on day one. My point is that people need to have social-economic choices that fit their situations. Better yet, once they get into a 30-year mortgage, they are not locked into that decision the entire time. As their finances improve, they can still choose to reduce their total cost of interest and the number of years until they own their home outright.

What mortgage solutions do you recommend? Please share with a comment.

Our weekly Ask Brian column welcomes questions from readers of all experience levels with residential real estate. Please email your questions or inquiries to [email protected].