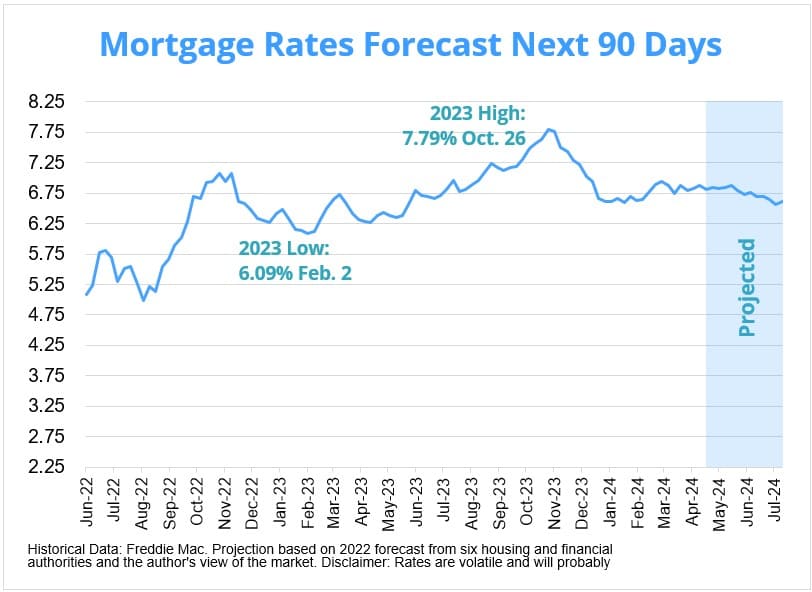

In this article, we'll explore the latest predictions for mortgage rates over the next 90 days. The next 90 days are unlikely to bring significant relief in mortgage rates. Economic conditions, inflation trends, and market sentiment suggest a relatively stable or slightly upward bias in rates. While a few months of improved inflation data could create space for rates to fall, the current outlook favors a scenario where mortgage rates remain within a narrow range.

Mortgage Rates Forecast for Next 90 Days

After a period of speculation regarding the trajectory of interest rates, the focus has shifted to whether rates will start to decline. The Federal Reserve's decision-making regarding the federal funds rate has significant implications for mortgage rates. However, other factors, such as inflation trends and economic indicators, also play crucial roles.

Factors Influencing Mortgage Rates

The anticipation of a potential decrease in the federal funds rate has led to speculation about mortgage rate movements. However, it's essential to recognize that a lower federal funds rate doesn't necessarily guarantee a proportional decline in mortgage rates. Several factors contribute to mortgage rate fluctuations:

- Inflation Trends: If inflation retreats and remains low, or if there's a softening in the economy or labor market, mortgage rates may decline.

- Government Debt: Record levels of government debt issuance can limit the extent to which mortgage rates can fall.

- Market Perception vs. Reality: Expectations regarding future monetary policy must align with economic realities for mortgage rates to adjust significantly.

Recent Trends

Recent market behavior reflects fluctuating expectations regarding the Federal Reserve's actions and economic indicators:

- Initial expectations of multiple rate cuts in 2024 led to a decline in mortgage rates.

- As expectations for rate cuts diminished, mortgage rates stabilized and even reversed slightly.

- Factors such as strong economic growth, robust labor markets, and persistent inflation pressures have influenced market sentiment.

Forecast for Next 90

Looking ahead to the next 90 days, several factors suggest that mortgage rates may not experience significant declines:

- Inflation Concerns: While inflation isn't worsening, it's not improving either, reducing the likelihood of substantial rate cuts from the Federal Reserve.

- Economic Outlook: Absent significant changes in economic indicators or labor market conditions, the potential for lower mortgage rates appears limited.

- Market Sentiment: Uncertainty surrounding future Fed policy and inflation trends makes it challenging for mortgage rates to move substantially higher or lower.

Will Mortgage Rates Go Down Next Month (June 2024)?

After a period of consistent increases, a recent dip in rates has sparked hope for a sustained decline. Let's delve deeper into the current climate and what experts predict for June 2024.

A Recent Respite:

May brought a welcome change after five weeks of rising mortgage rates. Freddie Mac reported a drop in the average 30-year fixed-rate mortgage to 7.09% by May 9th. This decline is attributed to signs of a potential economic slowdown, with a softening labor market and housing data playing a role.

The June Forecast: Buckle Up for Moderation

While a dramatic decrease seems unlikely, experts largely predict a period of moderation for mortgage rates in June, with most expecting them to hover within the low-to-mid 7% range. This prediction hinges on several key factors:

- The Inflation Rollercoaster: Inflation remains a central concern for the Federal Reserve. If May's inflation data shows no significant improvement, the Fed may be hesitant to cut rates, which could prevent a substantial drop in mortgage rates.

- Federal Reserve Policy in Focus: The Federal Reserve's approach to curbing inflation will heavily influence mortgage rates. While some speculate the Fed might ease up on rate hikes in June, others believe they'll maintain a “higher for longer” approach, keeping rates steady.

Expert Insights: A Spectrum of Opinions

Economists offer a range of forecasts for June mortgage rates, reflecting the complexities at play:

- Craig Berry (Acopia Home Loans) takes a nuanced approach. He acknowledges the Fed's intention to influence rates indirectly, suggesting that this might lead to dips later in June or July as the strategy unfolds.

- Molly Boesel (CoreLogic) adopts a cautious stance. While she doesn't foresee a significant drop, she believes rates will likely hold steady in the low-7% range due to lingering inflation concerns. This aligns with the predictions of other experts who prioritize the Fed's focus on inflation control.

- Ralph DiBugnara (Home Qualified) injects a note of optimism. He interprets the Fed's recent dovish tone as a sign that rates might hold steady in June. Additionally, he highlights the potential for future rate cuts inspired by other countries, which could lead to a more positive outlook for borrowers later in the year.

- Danielle Hale (Realtor.com) shares a conditional forecast. She predicts a possible decline towards 6.5% by year-end if inflation eases as expected. However, acknowledging the uncertain economic climate, she cautions that June might be too early to see the start of that trend. This perspective underscores the importance of staying informed about upcoming inflation data and the Fed's policy decisions.

- Odeta Kushi (First American) emphasizes the data-driven nature of the mortgage rate landscape. She foresees potential reductions if inflation continues its downward trajectory. However, she warns against expecting a quick drop if inflation remains stubbornly high. This highlights the importance of ongoing economic data analysis in predicting future trends.

- Rick Sharga (CJ Patrick Company) grounds his prediction in the Fed's wait-and-see approach. He believes rates will likely stay between 7.0-7.5% in June due to the central bank's cautious stance on cutting rates until they are confident that inflation is under control.

The Bottom Line: Stay Informed, Stay Prepared

While a significant decrease in June seems unlikely, a period of stability with some potential for slight fluctuations is more probable. Here are some key takeaways for homebuyers:

- Stay informed: Keep a close eye on inflation data and the Fed's policy decisions to anticipate future trends in mortgage rates.

- Budget for flexibility: Rate-test your budget for various mortgage rate scenarios (from 6.9% to 7.5%) to ensure affordability in this uncertain climate.

- Consider a mortgage broker: A qualified mortgage broker can help you navigate the complexities of the current market and secure the best possible rate for your situation.

By staying informed, preparing for various possibilities, and seeking professional guidance, you can make well-considered decisions as you navigate your homeownership journey.

Mortgage Interest Rates Forecast for the Next 90 Days

As inflation ran rampant in 2022, the Federal Reserve took decisive action to curb its effects, resulting in a spike in the average 30-year fixed-rate mortgage in 2023.

With inflation gradually cooling and the Fed adjusting its policies, including skipped hikes and expected cuts this year, the mortgage interest rates are poised for potential changes in the coming months. Moreover, with the economy exhibiting signs of slowing down, many experts anticipate a gradual descent in mortgage interest rates throughout 2024.

However, it's essential to recognize that rates are subject to fluctuation, and unforeseen global events can quickly disrupt economic stability, potentially leading to a rise in rates. As such, homebuyers and investors should remain vigilant and monitor market trends closely to make informed decisions regarding their mortgage plans in the next 90 days.

Mortgage rate predictions for 2024

As of April 11, the 30-year fixed-rate mortgage stood at 6.88%, according to data from Freddie Mac. However, projections from various housing authorities suggest that the average for the second quarter of 2024 will drop below this figure. All five major housing authorities surveyed anticipate that the average for Q2 2024 will be lower than 6.88%.

- Fannie Mae: Positioned at the lower end of the spectrum, Fannie Mae foresees the average 30-year fixed interest rate to settle at 6.3% for the second quarter.

- Mortgage Bankers Association (MBA), National Association of Realtors (NAR), and Wells Fargo: These organizations have a more optimistic outlook, projecting a slightly higher average of 6.6% for the same period.

These forecasts indicate a potential decline in mortgage interest rates compared to the recent 6.88% figure, providing potential relief for homebuyers and refinancers in the coming months.

| Housing Authority | 30-Year Mortgage Rate Forecast (Q2 2024) |

| Mortgage Bankers Association | 6.60% |

| National Association of Realtors | 6.60% |

| National Association of Home Builders | 6.61% |

| Wells Fargo | 6.65% |

| Fannie Mae | 6.70% |

| Average Prediction | 6.63% |

References:

- https://www.hsh.com/2month4cast.html

- https://www.noradarealestate.com/blog/mortgage-interest-rates-forecast/

- https://www.noradarealestate.com/blog/mortgage-rate-predictions-next-week/

- https://www.forbes.com/advisor/mortgages/mortgage-interest-rates-forecast/

- https://themortgagereports.com/32667/mortgage-rates-forecast-fha-va-usda-conventional