The savagely unhealthy housing market is continuing as we get closer to August. But, there is one bright spot — inventory is rising.

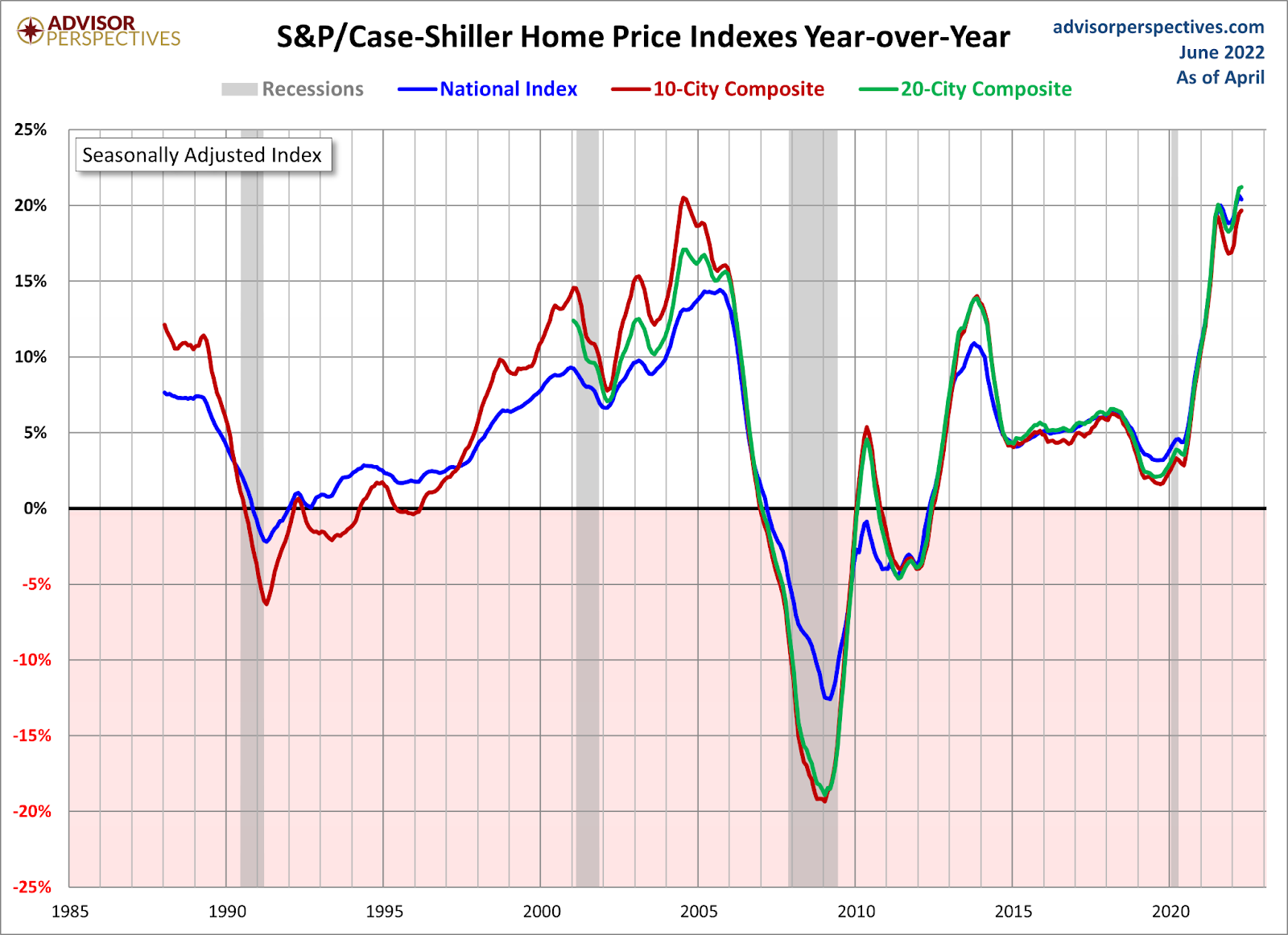

We still have the unhealthy dynamics of noticeable sales declines, but prices are still growing year over year. This has been a concern of mine after the summer of 2020 as inventory levels were breaking all-time lows, facilitating unhealthy home price growth during a more prominent demographic patch in U.S. history. The National Association of Realtors reported that existing home sales fell last month while prices increased yearly.

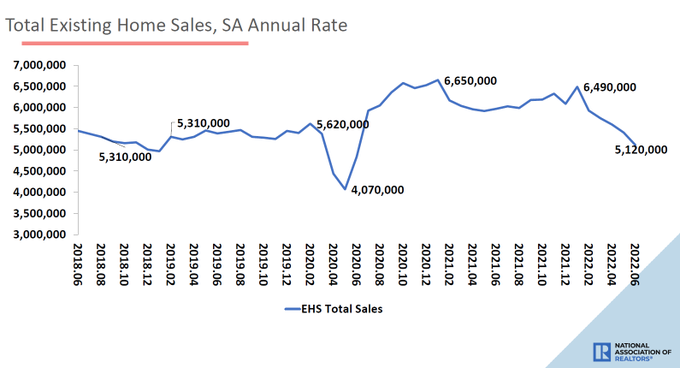

According to NAR, existing-home sales declined for the fifth straight month to a seasonally adjusted annual rate of 5.12 million. Sales were down 5.4% from May and 14.2% from one year ago. And, the median existing-home sales price climbed 13.4% from one year ago to $416,000, a new record high.

The one positive: Inventory is rising

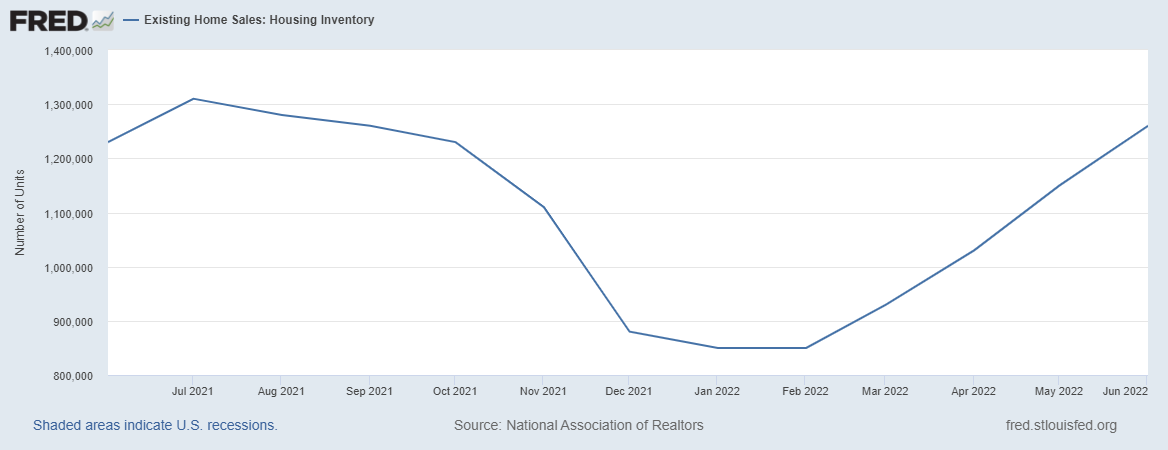

The one positive aspect of this report is that inventory is rising, which every American should be rooting for, because what we have experienced since 2020 was a historical housing inflation event. I have been talking about the range of inventory that I need to see to remove the ‘savagely unhealthy’ housing market theme. Once total inventory levels reach 1.52-1.93 million, we will be in a much better place for housing.

NAR total inventory data going back to 1982

Today’s report did show growth, which is the best part of the report, and let’s all hope for more inventory in 2023! A boring and balanced (B&B) housing market is the best housing market.

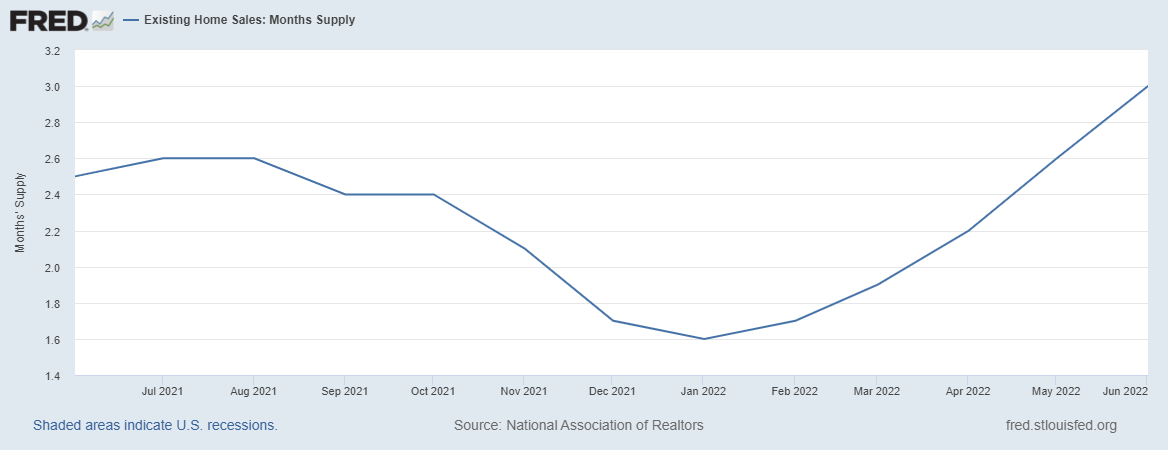

Total housing inventory registered at end of June was 1.26 M units, an increase of 9.6% from May and a 2.4% rise from the previous year (1.23 million). Unsold inventory sits at a 3.0-month supply at current sales pace, up from 2.6 months in May and 2.5 months in June ’21. #NAREHS

Here is the total inventory data updated with today’s report 1,260,000. I will be relieved once we can touch the 1,930,000 level. As long as rates stay high, we can get there next year.

Since the summer of 2020, I have believed that the housing market will change, but it does need the 10-year yield to break above 1.94% with duration.

This means 4%+ mortgage rates. The more significant issue is that during 2020-2024, I thought the housing market would be healthy as long as price growth stayed at 23% or under for those five years. The fear of inventory breaking toward all-time lows — with our demographics and low rates — was the biggest concern during this period.

That fear became a nightmare, because we broke above that critical cumulative price growth level in less than two years before 2022 arrived. Then, we started 2022 at all-time lows in inventory! Now you get the savagely unhealthy theme of 2022. I recently talked about this in an interview on Real Vision.

It seems odd that sales are declining but price growth is still climbing. This is common in recent history, which has happened before in 2013/2014 and 2018/2019. We had falling sales trends, but prices never went negative year over year. This is the unhealthy aspect of housing.

Higher rates work to cool down pricing, but for some natural balance, you need higher rates for a more extended period. In the past, when rates went up and cooled down demand, they fell back down again, making demand rise. The massive price increase we have seen since 2020 limits the power of lower rates, because home prices have held up in 2022 — a bit too strong in early 2022.

Higher rates need duration so sellers can adjust their pricing reality. This isn’t like the stock market, where you can sell your stock for a loss of 30% in seconds. Demand is getting softer and softer the longer rates stay higher.

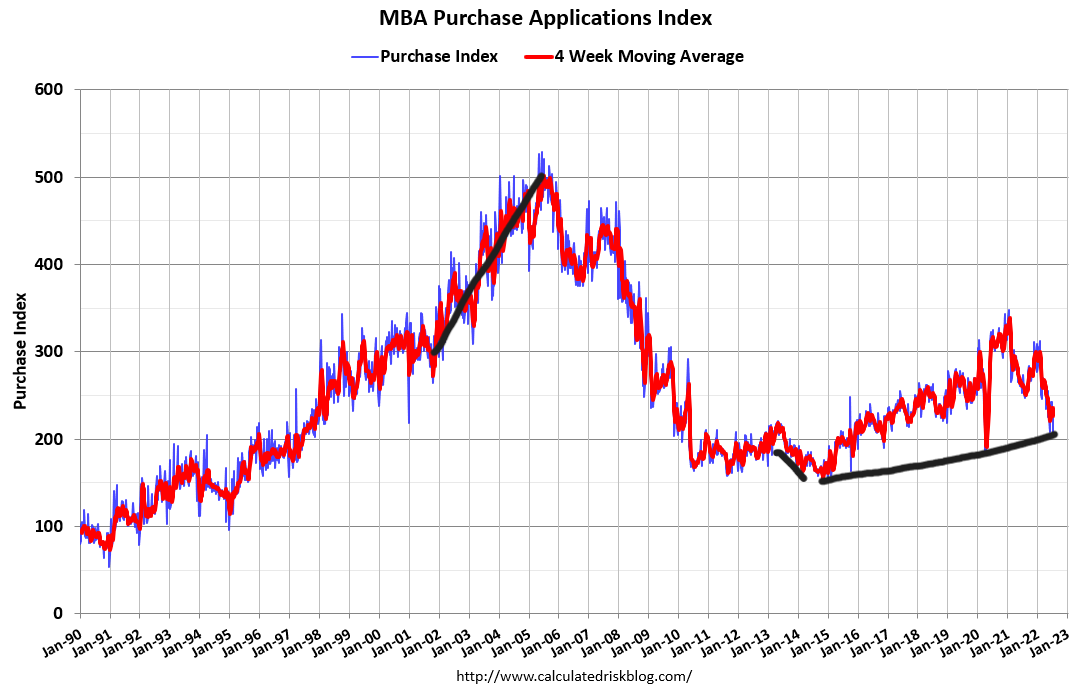

One thing I was wrong about early on, when rates rose, was that I believed the purchase application data would decline by 18%-22% on a four-week moving average earlier. Today is the first day that this has happened.

Purchase application data down

Purchase application data was down 7% weekly and 19% yearly. Today was the first day we broke into the 18%-22% range with a four-week average decline of 19.5%. We are already below 2008 levels today — not that far off the 21st century low of 2014. That year, purchase application data was down 20% year over year on trend, and it was the last time total inventory grew. We are roughly 1 million active listings below the peak of that year. However, we can see a clear demand-weakness trend in 2014 and 2022. It just held up better than I thought it would earlier in the year.

I had to figure out what I got wrong here, and I concluded that 4%-5% mortgage rates weren’t doing the damage I thought they would. The rise of adjustable-rate (ARM) loans helped mitigate the damage of higher rates. However, the year-over-year declines are picking up as rates are near 6%.

Pricing will change as inventory has picked up. The growth in pricing should cool. This will reverse only when mortgage rates go lower; however, as purchase application data show year-over-year declines, sales trends will head lower and lower.

@NAR_Research Total existing-home sales dipped 5.4% from May to a seasonally adjusted annual rate of 5.12 million in June. #NAREHS

Another negative item in this report — the days on market (DOM) are terrible. We want the DOM to get back above 30 days. In time, this should happen with higher rates and more inventory. However, you can see why pricing has held up in a savagely unhealthy way this year.

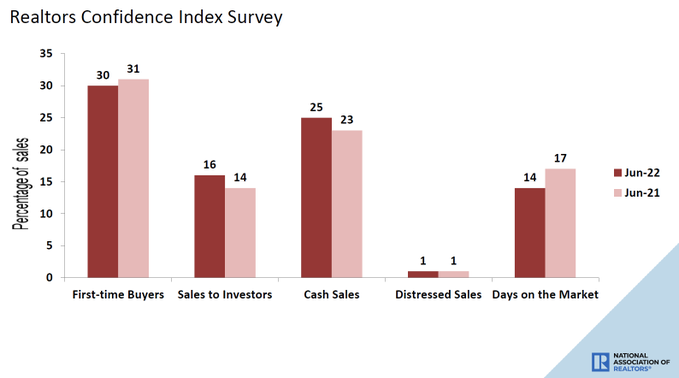

@NAR_Research First-time buyers were responsible for 30% of sales in June; Individual investors purchased 16% of homes; All-cash sales accounted for 25% of transactions; Distressed sales represented less than 1% of sales; Properties typically remained on the market for 14 days. #NAREHS

All in all, not a good report outside of inventory growing. My biggest fear is that my prediction of housing inflation taking off in a savagely unhealthy way has come true. Just imagine if mortgage rates didn’t rise toward 6% this year, we would have 15%-20% home price growth again.

In time, inventory will grow. Today, home buyers already have more choices than what they had last year. It’s a sad reality — we are in that “inventory broke to all-time lows” and it’s happening during this unique demographic patch in America. However, this is what we have to deal with right now. The market will get more balanced — it just needs time to get out of the savagely unhealthy mode.

Great article.

How many months of inventory does a 2022 housing market need? Is it four months rather than the traditional six months?

I’d love to know your opinion.

Thanks!

Four months of supply and 2019 total inventory are enough to be a balanced market. We had a balanced market in 2018/2019, When the inventory was at four months, and the entire inventory range was between 1.52 -1.93 nationally.

When we look at housing data post-1996, the only time we had six months + of supply was the 2006-2011 period on the existing home sales data.