Do you remember the good old days of pre-construction condominiums?

I do!

I remember when, among other things, you could purchase a pre-construction condo with a mere 5% deposit.

And that was it.

No further payments. Nothing due in 30 days. Nothing in 60 days, or 90 days, or 180 days. Nothing in a year.

Nothing upon occupancy, and nothing until the condominium was set to close and you obtained a mortgage of 95% for the remaining amount.

That was a long, long time ago.

It may as well be an eternity, based on how deposit structures work today, not to mention pricing.

When you could buy a bachelor condo at The Met for $99,000, with only 5% down, the comparable unit across the street in a 15-year-old building was worth $150,000.

Your profit was already factored in, irrespective of market appreciation.

That was the reason to buy pre-construction condos back in 2004, not to mention that absurd 5% deposit structure.

I remember when deposits hit 10%. It was only a matter of time, really.

And when the Financial Crisis of 2008 shocked the world (except for Canada, of course…) developers started looking for 15% deposits.

Back then, the posted deposits weren’t always carved in stone.

I bought into a development in 2005 where deposits were 15% total, with 5% payable at 30 days, 180 days, and 365 days, only I was able to get away with a 10% total, providing 2.5% after 90 days, 180 days, 365 days, and 730 days.

The prices were so cheap that it wasn’t about the cash flow needed after 30 days as opposed to 90 days, but rather I was questioning whether the development would get off the ground. Plus, why pay the extra 5% if you don’t have to?

Somewhere along the way, developers started to require 20% deposits, and I think that was a direct result of the 2008 Financial Crisis and the banks wanting to know that buyers could actually come up with a 20% down payment well in advance of actually needing to close.

Keep in mind, this was back when you could still purchase a resale property for as high as $999,999 with only a 5% down payment. Not deposit, folks, but down payment.

We’re talking about buying for just shy of $1,000,000 and putting down only $50,000, and obtaining a mortgage for $950,000.

Today, we have a sliding scale that requires 5% on the first $500,000 and 10% on the next $500,000, meaning a 7.5% down payment on a purchase of $999,999.

But I’ll do you one better: there was a time when you could purchase a resale property over $1,000,000 with only 5% down.

And yet all the while, pre-construction condominium developers were requiring deposits of 20%?

That made no sense to me.

I mean, it made sense from the developers’ viewpoint, but not if I were looking at this as a buyer.

Today, the deposits are almost exclusively 20%.

They might be structured differently, and once in a while, the structures might be negotiable, but the 20% typically needs to be submitted within the first 180 – 360 days.

That is, until now.

As you likely assumed from the title of today’s blog, there’s a new game in town!

Maybe this isn’t so new, but it hit my inbox the other day and I found it rather interesting.

These “offers” are being provided by a registered real estate brokerage, so I can’t share everything or the brokerage and/or agents could have a RECO claim against me.

So let’s just start with the subject line in the email:

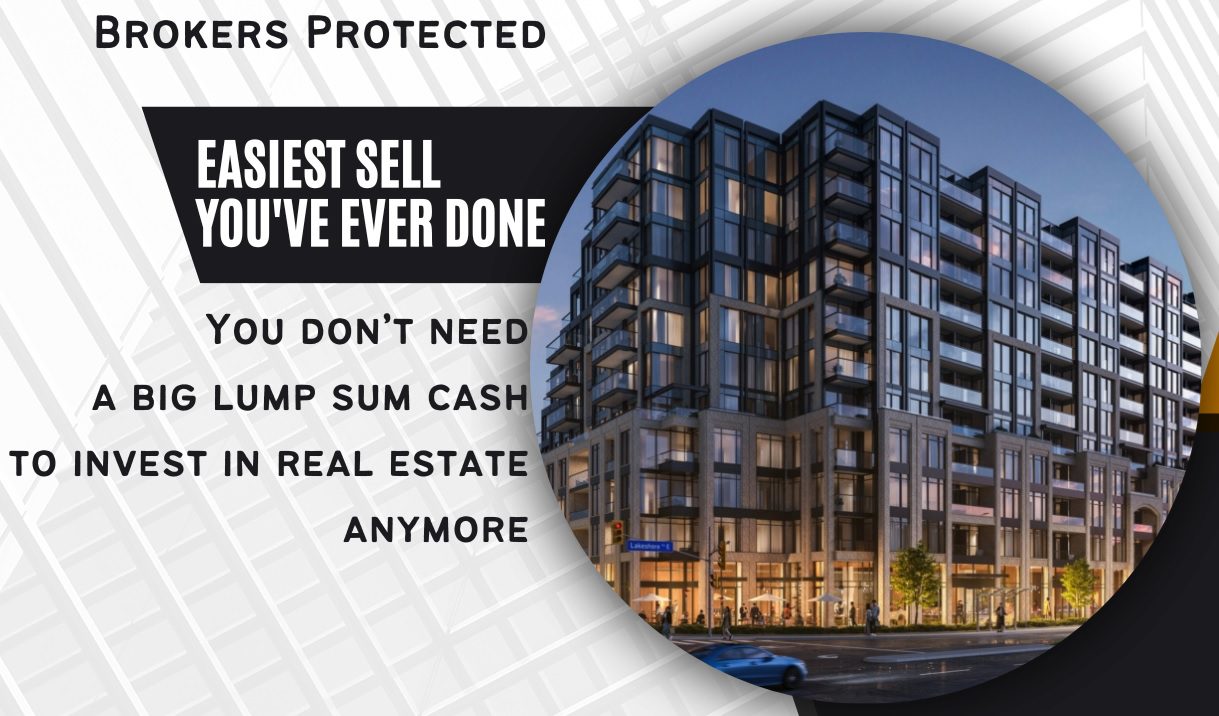

David, Easiest sell you’ve ever done with our BULK PRE-NEGOTIATED DEAL

While they were able to format their email blasts so my name is included, we’re not off to the best start when it comes to grammar since this reads “sell” instead of “sale.”

They also seemed to get their keyboard stuck on CAPS LOCK, or, maybe they just thought that was classy.

Then this caught my eye:

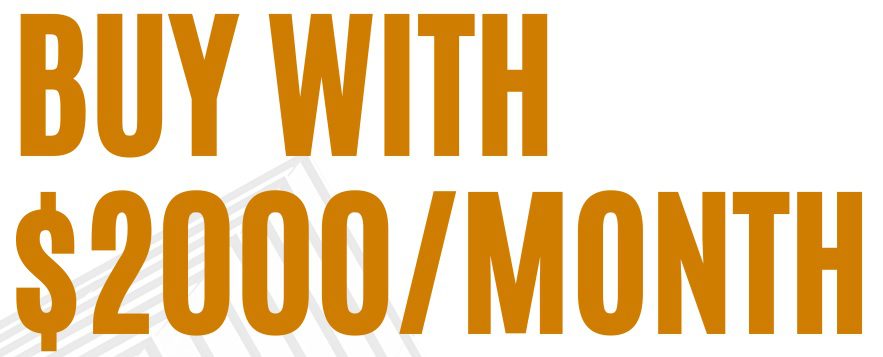

And to think, this whole time, I’ve been unaware that buying pre-construction condos in Mississauga on the installment plan was going to take me to the promised land.

There’s a lot of selling in this email, and I have to think there’s a certain demographic they’re trying to attract.

The colours, the fonts, the verbiage – it reeks of low-end sales tactics, all around.

I’ve seen high-end pre-construction sales and classy brouchures, salesmanship, and sales people.

But this is something different:

It sounds way, way too “salesey” to me, but what do I know?

There’s a buyer for everything!

Maybe some people won’t question the concept of “pre-negotiated bulk deals” or how they work, what the discount is, and who’s at the helm.

I hate the message here. Whether it’s the different colours, fonts, or the words being used, it’s just gross.

But the best is yet to come.

Consider that, to some extent, all pre-construction sales are on the “installment plan,” since you pay 5% within 30 days, then another 5% at 180 days, and so on. But when I think about four payments of 5% staggered across one year, I consider this more of a “deposit structure” than an “installment plan.”

When I think “installments” or “installment plans” I think about three easy payments from the infomercials.

And if you’re selling real estate, you don’t want to be associated with Ron Popeil’s Pasta Maker…

If you’re my age, you will freely admit that you’ve watched the entire infomercial, start-to-finish.

“Set it, and…….”

So where’s the comparison as far as pre-construction condominiums are concerned?

It’s in this section of the email, here:

And that, folks, is where we’ve officially gone from “deposit structures” to “installment plans.”

You might be quick to point out that this can work for some people or that it’s more advantageous.

Instead of paying $24,000 in 365 days, some might prefer to spread those payments out and provide a deposit of $2,000 per month.

However, I would then argue that the people who are doing this are the ones that don’t trust themselves to come up with $24,000 at the end of the year, and thus they choose to pay $2,000 per month. And as a result, I would argue that these people shouldn’t be buying pre-construction condos.

Here’s another beauty:

“Easiest Sell You’ve Ever Done” is also not grammatically correct.

But who cares about attention to detail, right?

Especially when you “Dont Need A Big Lump Sum Cash To Invest In Real Estate Anymore,” which is, ironically, also not grammatically correct.

Raise your hand if you remember eight minute abs.

Any hands raised?

Eight-minute abs was huge back in the day! The idea of getting ripped abs in only eight minutes had huge appeal and this spawned all sorts of television shows, books, workout videos, and merchandise.

If you were lucky, you had this videocassette at home:

Boom!

Nothing beats 8-minute abs.

Nothing!

Except, wait…

…what if there was a way to do it even quicker?

Like, perhaps:

Good lord!

You can’t do abs in seven minutes!

Eight minutes, fine. No problem.

But seven minutes? Who comes up with this?

So, imagine my shock and awe as I’m sitting in my office on Sunday afternoon of the long weekend and I open up an email.

Fresh off the idea for this blog post, with the offer of buying pre-construction condos for only $2,000 per month, I’m presented with this:

Damn, Gina!

Only $60………per day?

That, folks, is how you beat 8-minute abs. Er, I mean, that is how you beat $2,000 per month.

And best of all, it’s a “FIRE SALE.”

Because when you think to yourself, “safe, long-term investment, no impulse, no gimmicks, well researched and well-thought-out,” you can’t help but feel all your boxes are checked when you read “FIRE SALE.”

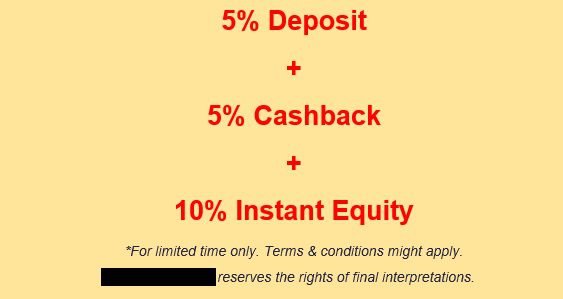

And the math on the investment is totally sound:

I think there’s supposed to be an equals sign instead of that second plus sign, as in a 5% deposit + 5% cashback = 10% instant equity, but who really knows when it comes to this development and sales team.

Not only that, if somebody told you that after providing a 5% deposit, you would get 5% cashback, would you believe it? Or would you be smart enough to know that they’re simply charging 5% more for the end product?

The definition of “equity” seems to be escaping these folks, even if the 5% cashback came from a money-tree. It’s still not right.

In any event, this seems to be the way that the pre-construction condominium industry is heading; at least with the less popular, tougher-to-sell projects out there.

The developers are allowing certain brokerages and agents, who aren’t “in-house,” to advertise their projects and this is the end result.

But I’m not complaining.

Because how else would I be able to write a blog post and include references to eight-minute abs?

Somewhere, Harland Williams and Ben Stiller are with me…

Libertarian

at 9:18 am

“Who works out in six minutes.”

“Seven is the key number here.”

Harland Williams was hilarious back in the day. And that movie was as well. Classic Farrelly brothers. David, thanks for the trip down memory lane.

Different David

at 10:25 am

David, sorry to call you out, but “Set it and forget it!” was Ron Popeil’s rotisserie oven.

The pasta maker was great, I was always secretly hoping that my parents would buy it. But really, after thinking about it, pasta was probably less than $0.50 per package back then. So you need to make 240 pasta dinners (plus the cost of the ingredients and shipping and handling) to break even.

Anyone for spray on hair?

Vancouver Keith

at 6:01 pm

I wish I could make a more specific comment, but I’ll simply point out that the economic history of increasingly complex ways of borrowing and investing is full of tears. So far, the federal government has been backstopping real estate valuations in ways large and small through thick and thick. Should a day of reckoning arrive, the economic carnage will be vast.

Ace Goodheart

at 7:00 am

Little public service announcement for all the young folks who think socialism is the way to home ownership (its nor, in socialist countries the government owns all the houses):

All the spare parts are coming together for what looks to be a sharp downward correction in generalized home prices in Canada.

If you play this right, you could even be living detached in Toronto with some nice equity.

Here’s what you do:

1. Don’t buy now. You want to buy in mid 2026

2. Start saving your down payment. GIC rates are currently over 5%. Inflation is on its way down to 2% and will stay there. Interest rates are rising. Buy GICs that mature mid 2026

In 2026 housing will be seen as a risky bet. People will have lost their shirts. Everyone will be scared of it. Interest rates will be headed down and banks will be pushing out mortgages to try to drum up business.

You’ll have big bucks from saving stashed away in GICs that beat inflation every year you had them.

Buy your house in a falling, nervous market. You’ll get a good deal.

Then just ride the value back up again as the economy improves, Interest rates fall and equity builds.

If you do that, you’ll have done what I did and successfully predicted the future. Crystal balls are real and right now you can easily see three years out.

Oh and stop electing socialists.

Please.

Different David

at 8:50 am

Thanks Ace.

Perhaps a GIC that matures in 2025 so that you have liquid cash available to buy Canadian bank stocks after a Conservative win?

Ace Goodheart

at 9:18 am

I would say 2026. That seems to be the year for house buying.

The Libs are about to introduce their “online harms bill” which is going to peeve off the younger folks who like to do whatever they want on the internet (young folks could care less about pretty much everything, EXCEPT their online habits. They live online. This is the final nail in the coffin for the Trudeau Liberals. They are about to become the most hated government in the world with this one).

So with what looks to be an almost bought and paid for Conservative majority in 2025, I look at what caused high house prices in the first place.

All the needles point to the Federal government exercising control over our Central Bank. In any country where the Central bank has lost its independence from the government, you see asset bubbles. In Venezuela when that happened, the price of a used car went to five figures and then higher. You can’t print houses.

Now that our Central bank has regained its independence and is once again working as it should, the air is coming out of the various asset bubbles that were created. One of those bubbles is housing.

Now, in 2025-2026 all those folks with 1.2% mortgages and 90 year amortization periods, have to renew at north of 7% for a 25 year term. They are going to get blown out of the water. And the Conservatives are not going to help them. Sink or swim is the Conservative motto. We don’t throw you a life line. People need to help themselves.

So the intelligent young person who saw this coming, stashed away a down payment in GICs which are approaching 6%, while inflation is heading back down to 2%. They avoided high interest rates, and sat on the back side of the rate curve, sucking up equity as others floundered. They then enter the market on the downturn, when people are tossing houses aside like they are on fire and they don’t want to get burned. They pick up a cheap mortgage as rates decrease and the Central bank tries to stimulate a dying economy.

It is perfect. And very predictable.

This is how you make bank in real estate. Not by electing socialist governments.

David Fleming

at 10:50 am

@ Ace Goodheart

I don’t believe the Conservatives will win a majority in 2025.

I also don’t believe they will win, period.

Canadians have demonstrated that they prefer the devil they know versus the devil they don’t.

Ace Goodheart

at 11:42 am

You may be right.

However, my experience with voting in Canada is that people vote against governments, not for them.

At the moment, there is not enough support for a “throw the bums out” movement against the Liberals. But that support is building. Once it does, it doesn’t matter if the Conservatives are running a three legged donkey as leader, they win anyway.

As soon as there is a generalized rejection of the Libs, Trudeau and all that they stand for, the Conservatives will win. That is going to happen soon, from what I am seeing.

Vancouver Keith

at 2:07 pm

Interesting take. Problem with history is that it doesn’t repeat. I look at the Liberal/NDP coalition and I see that 40% of Canadians don’t pay federal income tax net of benefits. I view the political center in Canada as having shifted to the left in the last decade.

It remains to be seen if Pierre Poilievre can a) unite enough of the Canadian right wing, and b) overcome the Liberal and NDP brand of negative campaigning on Conservative platform both real and imagined. A couple of tall orders. Liberals aren’t a lot of things, sadly for Canadians but they are highly skilled at politics and campaigning. The coming election will be a big test of the current Conservative party, we’ll see what they’ve learned from last time.

Ace Goodheart

at 12:34 pm

RE: Vancouver Keith:

I think the Libs will lose support of the young folks with their online harms bill and the associated “war” they are having right now with various US based online giants.

The idea seems to be that the CRTC will “regulate” what a Canadian young person is allowed to post, and view, on the internet.

If you have a look at even all ages content available on YouTube right now, you immediately see the problem with this. The CRTC will have issues with pretty much every social media influencer. Every YouTube celebrity. There is just so much “wrong” with what is going on in the cyberspace right now, from the viewpoint of a professional regulator.

But will the young folks accept this? Or will they form a “throw the bums out” anti Liberal movement? The old folks already are losing faith in the Libs (they are going after our houses and our retirement savings). But young people love them. Will that continue to be the case, if the Libs roll out a nanny state online “big brother has to approve your internet habits” type regulation system?

For me, I could care less. I use the internet for reading mainstream blogs (like this one), searching for classic cars (still looking for my elusive 1973 VW thing which apparently they don’t have any for sale in all of Canada), and reading mainstream news. So they can regulate me all they like. I don’t mind.

But young people? I don’t think this is going to work. What about all the Canadian social media influencer and influencer wannabees? What about all the consumers of US based YouTube, TikTok, and other online media platform content that will soon be banned?

Oh I think there is going to be a problem with that. Young folks are going to be peeved.