Housing inventory finally hit my target level of growth last week with mortgage rates now over 7.25%, something I couldn’t get all last year. Of course, what is different this year versus last year is that new listing data is growing yearly instead of trending at the lowest levels recorded in history. This is something I talked about last week on Yahoo Finance.

Weekly housing inventory data

Higher mortgage rates with duration will likely lead to higher inventory, which we have seen repeatedly for the past 10 years. However, 2023 tested my model as the inventory growth rate on a week-to-week basis was slow, even when rates headed toward 8%. It’s a simple model: inventory should grow between 11,000-17,000 weekly with rates over 7.25%. After failing time and time again, we finally got there this week with 16,582.

- Weekly inventory change (April 12-19): Inventory rose from 526,462 to 543,044

- The same week last year (April 14-21), Inventory rose from 406,600 to 414,701

- The all-time inventory bottom was in 2022 at 240,194

- The inventory peak for 2023 was 569,898

- For some context, active listings for this week in 2015 were 1,060,669

New listings data

Now that inventory is growing more closely with what I am looking for, new listing data must keep its year-over-year growth trend. Last year, when mortgage rates headed toward 8%, we saw no negative hit to the latest listings data, meaning it didn’t take a new leg lower. So, with higher rates now and some growth year over year, I hope we keep the momentum going. We need this to happen to get balance in housing.

Here’s what new listings look like for last week over the last several years:

- 2024: 68,769

- 2023: 59,269

- 2022: 59,803

Price-cut percentage

In an average year, one-third of all homes take a price cut; this is standard housing activity. When mortgage rates increase, demand falls and the price-cut percentage grows. That percentage falls when rates drop and demand improves.

As mortgage rates rise with inventory, the price-cut percentage should increase unless demand keeps up with inventory growth. Last week, we saw a slight decline in the price cuts.

Here is the price-cut percentage for last week over the last several years:

- 2024: 32%

- 2023: 29.4%

- 2022: 18.7%

10-year yield and mortgage rates

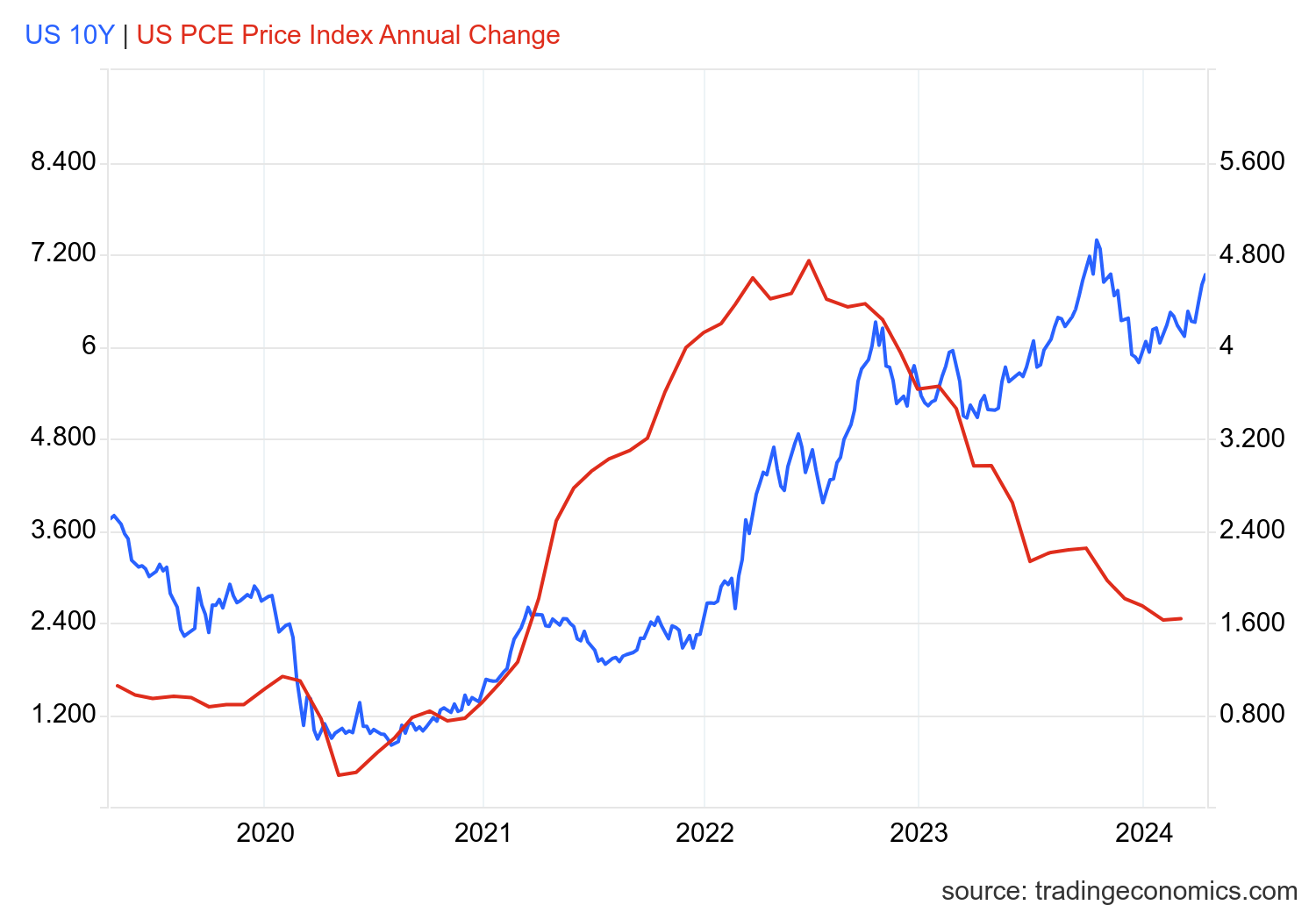

We had a lot of headline drama last week, between Powell talking about taking rate cuts off the table, escalating war in the Middle East, and economic data beating estimates. This sent the 10-year yield and mortgage rates higher. I talked about this on the HousingWire Daily podcast, discussing my central theme that for the Fed to pivot, it’s labor over Inflation.

When the labor market breaks, the Fed will pivot; we aren’t there just yet. As the chart below shows, many people were looking at the growth rate of inflation falling as the main driver for the Fed, but that isn’t working in this cycle.

One positive story about mortgage rates in 2024 is that the spreads are improving, and that has kept a lid on the damage from higher yields. The spreads are acting a bit better than I thought they would, I had assumed we would need to get closer to rate cuts before they would behave this way. However, this bodes well for the future because if the spreads get back to normal and the 10-year yield falls with it, we can easily get to the low 6s range for mortgage rates and potentially below 6%.

Purchase application data

One surprising data point from last week was that purchase application data showed positive growth, and the year-over-year decline was much less.

However, the only reason this happened is that the week before, the Easter holiday negatively impacted the data, which made this week’s growth data need a lot of context. With weekly housing data, holiday activity can move negative and positive, but after two weeks, it gets back on trend. So, take last week’s growth with a grain of salt.

Since November 2023, when mortgage rates started to fall, we have had 11 positive prints versus seven negative prints and two flat prints week-to-week. Year to date, we have had five positive prints, seven negative prints, and two flat prints.

The week ahead: Housing and inflation

We have new home sales and pending home sales coming up this week, and we will see how much the recent rate increase has impacted the data line. Also, the Fed’s main inflation report, the PCE inflation data, will be released on Friday, so it should be a wild day. Ever since the 10-year yield broke it’s critical support line, the bond market and mortgage rates have been acting up, so this inflation report will be key as the Fed will factor in how much we need mortgage rates to stay higher for longer in this economic expansion.