How to pick the best home improvement loans for your project

Home improvement loans offer a financial solution to the often expensive nature of home renovations, allowing you to fund upgrades and repairs without the immediate out-of-pocket expense.

Some, like the FHA 203(k) mortgage, are specialized for home renovation projects, while second mortgage options, like home equity loans and HELOCs, can provide cash for a remodel or any other purpose.

Your best financing option for home improvements depends on your needs. Here’s what you should know.

Check home improvement loan options and rates. Start hereIn this article (Skip to...)

- Types of home improvement loans

- How to choose a loan

- Home improvement loan rates

- Home improvement loan lenders

- Qualifying for home improvement loans

- FAQ

What is a home improvement loan?

Home improvement loans are an ideal solution for covering the costs of major home repairs or renovation projects. Whether you’re planning a comprehensive overhaul or simply updating a single room, these loans provide the financial support you need.

They come in handy for improvements that uplift your living experience, such as installing energy-efficient windows, modernizing electrical systems, or upgrading to a contemporary bathroom design. Owning a home comes with its fair share of challenges, especially when it comes to maintenance and renovations.

The costs can quickly escalate, often reaching into the tens of thousands. Yet, these investments in your home can be worthwhile. Thoughtful renovations like transforming an attic into a functional living space, landscaping your garden to enhance curb appeal, or fitting a state-of-the-art kitchen can appreciably increase the value of your property.

Home improvement loans vs home renovation loans

Now, you might be wondering how this is different from a home renovation loan. While the terms are often used interchangeably, there can be subtle differences.

Home improvement loans are generally more flexible and can be used for any type of home project, from installing a new roof to landscaping. Home renovation loans, on the other hand, are often more specific and may require you to use the funds for particular types of renovations, like kitchen or bathroom remodels.

How do home improvement loans work?

So, you’ve decided to spruce up your home, and you’re considering a home improvement loan. But how do they work? Once you’re approved, the lender will give you the money in a lump sum. You start repaying the loan almost immediately, usually in fixed monthly installments. The interest rate you’ll pay depends on various factors, including your credit score and the lender’s terms.

Be mindful of additional costs like origination fees, which can range from 1% to 8% of the loan amount. Unlike a credit card, where you can keep using the available credit as you pay it off, the loan amount is fixed. If you find that you need more money for your project, you’ll have to apply for another loan, which could affect your credit score.

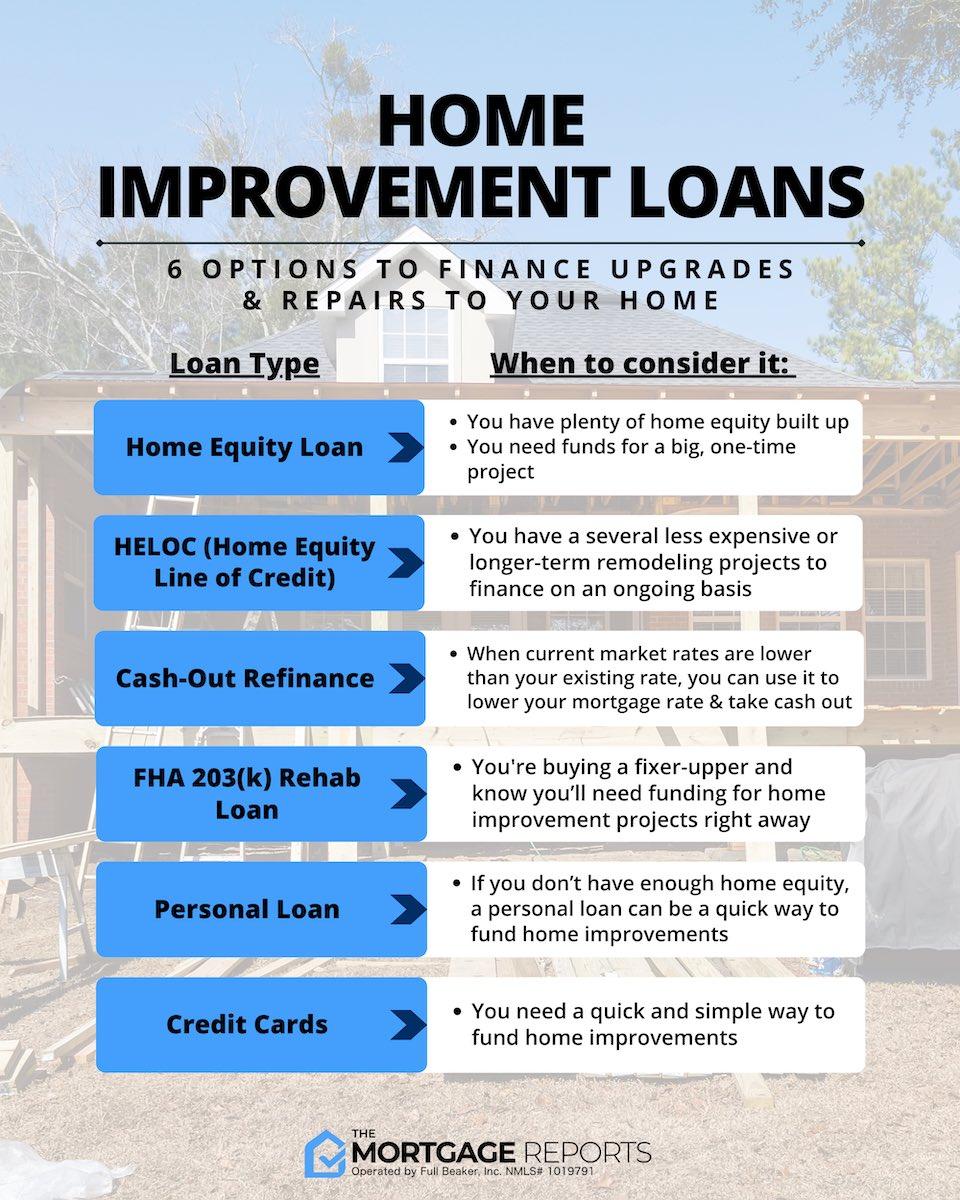

Types of home improvement loans

Most borrowers will have a choice between five types of home improvement loans. While all are viable options for home improvement financing, some may be better suited to your needs than others. There’s a sixth alternative available to homeowners in need of emergency repairs. And that’s a credit card. While it is not the ideal option for everyone, there are some unexpected benefits to taking this route.

Here’s what you should know about the various types of home improvement loans.

1. Home equity loan

You can borrow money using the equity you have accrued in your house as collateral through a home equity loan (HEL). You can calculate your home equity by subtracting your existing mortgage loan balance from your current home value.

Unlike a cash-out refinance, a home equity loan “issues loan funding as a single payment upfront. It’s similar to a second mortgage,” says Bruce Ailion, a Realtor and real estate attorney. “You would continue making payments on your original mortgage while repaying the home equity loan.”

Check home equity loan options and rates. Start hereThis type of home improvement loan is particularly useful for big, one-time expenditures like home remodeling. It offers a fixed interest rate, and the loan terms can range from five to 30 years. You could potentially borrow up to 100% of your home’s equity.

There are a few drawbacks, though. Since you’re essentially taking on a second loan, you’ll have an additional monthly payment if you still have a balance on your original mortgage. Also, the lender will usually charge closing costs ranging from 2% to 5% of the loan balance, as well as potential origination fees. Because the loan provides a lump-sum payment, careful budgeting is necessary to ensure the funds are used effectively.

As a bonus, “a home equity loan, or HELOC, may also be tax-deductible,” says Doug Leever with Tropical Financial Credit Union, member FDIC. “Check with your CPA or tax advisor to be sure.”

2. HELOC (home equity line of credit)

A Home Equity Line of Credit (HELOC) is another option for tapping into your home’s equity without going through the process of a full refinance. Unlike a standard home equity loan that provides a lump sum upfront, a HELOC functions more like a credit card. You’re given a pre-approved limit and can borrow against that limit as you need, paying interest only on the amount you’ve actually borrowed.

Check your HELOC options. Start hereWhile there’s more flexibility because you don’t have to borrow the entire amount at once, be aware that by the end of the term, “the loan must be paid in full. Or the HELOC can convert to an amortizing loan,” says Ailion. “Note that the lender can be permitted to change the terms over the loan’s life. This can reduce the amount you can borrow if, for instance, your credit goes down.”

The pros of a HELOC include minimal or potentially no closing costs and loan payments that vary according to how much you’ve borrowed. It offers a revolving balance, which means you can re-use the funds after repayment. This type of home improvement loan may be ideal for ongoing or long-term projects that don’t require a large sum upfront.

“HELOCs offer flexibility, and you only pull money out when needed, within the maximum loan amount. And the credit line is available for up to 10 years, which is your repayment period.” Leever says.

3. Cash-out refinance

A cash-out refinance is a viable option if you’re considering home improvements or other significant financial needs, like debt consolidation. Opting for a cash-out refinance involves taking on a new, larger mortgage than your existing one and then pocketing the difference in cash.

This cash comes from your home’s value and can be used for various purposes, including home improvement projects like finishing a basement or remodeling a kitchen. However, the money can also be used for other things, like paying off high-interest debt, covering education expenses, or even buying a second home. Doing a cash-out refinance is most beneficial when current market rates are lower than your existing mortgage rate.

Check your eligibility for a cash-out refinance. Start hereThe advantages of going for a cash-out refinance include the opportunity to reduce your mortgage rate or loan term, which could potentially result in paying off your home earlier. For instance, if you initially had a 30-year mortgage with 20 years remaining, you could refinance to a 15-year loan, effectively paying off your home five years ahead of schedule. Plus, you only have to worry about one mortgage payment.

However, there are downsides. Cash-out refinances tend to have higher closing costs that apply to the entire loan amount, not just the cash you’re taking out. The new loan will also have a larger balance than your current mortgage, and refinancing effectively restarts your loan term length.

4. FHA 203(k) rehab loan

The Federal Housing Administration backs the FHA 203(k) rehab loan, which combines the costs of a home mortgage and home improvements into a single loan. It’s particularly useful for people buying fixer-uppers.

Check your eligibility for an FHA 203(k) loan. Start hereWith this program, you don’t need to apply for two different loans or pay closing costs twice; you finance both the house purchase and the necessary renovations at the same time. The loan comes with several benefits, like a low down payment requirement of just 3.5% and a minimum credit score requirement of 620, making it accessible even if you don’t have perfect credit. Additionally, first-time home buyer status is not a requirement for this home remodel loan.

However, there are some limitations and downsides to be aware of. The FHA 203(k) loan is specifically designed for older homes in need of repairs, rather than new properties. The loan also includes both upfront and ongoing monthly mortgage insurance premiums. Renovation costs have to be at least $5,000, and the loan restricts the use of funds to certain approved home improvement projects.

According to Jon Meyer, a loan expert at The Mortgage Reports, “FHA 203(k) loans can be drawn out and difficult to get approved. If you go this route, it’s important to choose a lender and loan officer familiar with the 203(k) process.”

5. Unsecured personal loan

If you’re looking to finance home improvements but don’t have sufficient home equity, a personal loan could be a suitable option. Unlike home equity lines of credit (HELOCs), personal loans are unsecured, meaning your home is not used as collateral. This feature often allows for a speedy approval process, sometimes getting you funds on the next business day or even the same day.

Check home improvement loan options and rates. Start hereThe repayment terms for personal loans are less flexible, usually ranging between two and five years. Although you’ll most likely face closing costs, personal loans can be easier to access for those who don’t have much home equity to borrow against. They can also be a good choice for emergency repairs, such as a broken water heater or HVAC system that needs immediate replacement.

However, there are notable downsides to consider. Unsecured personal loans generally have higher interest rates compared to HELOCs and lower borrowing limits. The short repayment terms could put financial strain on your budget. Additionally, you may encounter prepayment penalties and expensive late fees. Financial expert John Meyer describes personal loans as the “least advisable” option for homeowners, suggesting that they should be considered carefully and perhaps as a last resort.

6. Credit cards

Using a credit card can be the fastest and most straightforward way to finance your home improvement projects, eliminating the need for a lengthy loan application. However, you’ll need to be cautious about credit limits, especially if your renovation costs are high.

You might need a card with a higher limit or even multiple cards to cover the costs. The interest rates are generally higher compared to home improvement loans, but some cards offer an introductory 0% annual percentage rate (APR) for up to 18 months, which can be a good deal if you’re sure you can repay the balance within that time frame.

Check home improvement loan options and rates. Start hereCredit cards might make sense in emergency situations where you need immediate funding. For longer-term financing, though, they’re not recommended. If you do opt for credit card financing initially, you can still get a secured loan later on to clear the credit card debt, thus potentially saving on high-interest payments.

How do you choose the best home improvement loan for you?

The best home improvement loans will match your specific lifestyle needs and unique financial situation. So let’s narrow down your options with a few questions.

Check your home improvement loan options. Start hereDo you have home equity available?

If this is the case, taking out a home equity loan, home equity line of credit, or cash-out refinance are your best options for obtaining the lowest rates.

Here are a few tips for choosing between a HELOC, home equity loan, or cash-out refi:

- Can you get a lower interest rate? If so, a cash-out refinance could save money on your current mortgage and your home improvement loan simultaneously.

- Are you doing a big, single project like a home remodel? Consider a simple home equity loan to tap into your equity at a fixed rate.

- Do you have a series of remodeling projects coming up? When you plan to remodel your home room by room or project by project, a home equity line of credit (HELOC) is convenient and worth the higher loan rate compared to a simple home equity loan.

Are you buying a fixer-upper?

If so, check out the FHA 203(k) program. This is the only loan on our list that bundles home improvement costs with your home purchase loan. Just review the guidelines with your loan officer to ensure you understand the disbursement of funds rules.

Taking out just one mortgage to cover both needs will save you money on closing costs and is ultimately a more straightforward process.

“The only time I’d recommend the FHA203(k) program is when buying a fixer-upper,” says Meyer. “But I would still advise homeowners to explore other loan options as well.”

Do you need funds immediately?

When you need an emergency home repair and don’t have time for a loan application, you may have to consider a personal loan or even a credit card.

Which is better?

- Can you get a credit card with an introductory 0% APR? If your credit history is strong enough to qualify you for this type of card, you can use it to finance emergency repairs. But keep in mind that if you’re applying for a new credit card, it can take up to 10 business days to arrive in the mail. Later, before the 0% APR promotion expires, you can get a home equity loan or a personal loan to avoid paying the card’s variable-rate APR.

- Would you prefer an installment loan with a fixed rate? If so, apply for a personal loan, especially if you have excellent credit.

Just remember that these options have significantly higher rates than secured loans. So you’ll want to reign in the amount you’re borrowing as much as possible and stay on top of your payments.

Home improvement loan rates

Interest rates for home improvement loans can vary widely, generally ranging from 5% to 36%. Your credit score plays a significant role in determining your rate—the better your credit, the more favorable your rate. Some lenders even offer an autopay discount if you link a bank account for automatic payments.

Find your best home improvement loan rate. Start hereYou can also prequalify to check your likely interest rate without affecting your credit score, making it easier to plan for the loan purpose, whether it’s a new kitchen or fixing a leaky roof.

So, whether you’re dreaming of solar panels or finally fixing up your master bedroom, a home improvement loan can be a practical way to finance your projects. Just make sure to read the fine print and understand all the terms, including any potential autopay discounts and bank account requirements, before you apply.

Home improvement loan lenders

When considering a home improvement loan, it’s necessary to explore various lending options to find the one that best suits your needs. The lending landscape for home improvement is diverse, featuring traditional banks, credit unions, and online lenders. Each type of lender offers different interest rates, loan terms, and eligibility criteria.

Compare quotes from multiple lenders at once. Start hereIt’s advisable to prequalify with multiple lenders to get an estimate of your loan rates, which generally doesn’t affect your credit score. This way, you can compare offers and choose the most favorable terms for your renovation project.

Among the popular choices in the market, Sofi and LightStream stand out for their competitive rates, easy online application, and customer-friendly terms. Both lenders are equal housing lenders and adhere to federal anti-discrimination laws. In addition to these, other lenders like Wells Fargo and LendingClub also offer home improvement loans with varying terms and conditions.

How to get a home improvement loan

Getting a home improvement loan is similar to qualifying for a mortgage. You’ll want to compare rates and monthly payments, prepare your financial documentation, and then apply for the loan.

Check home improvement loan options and rates. Start here1. Check your financial situation

Check your credit score and debt-to-income ratio. Lenders use your credit report to establish your creditworthiness. Generally speaking, lower rates go to those with higher credit scores. You’ll also want to understand your debt-to-income ratio (DTI). It tells lenders how much money you can comfortably borrow.

2. Compare lenders and loan types

Gather loan offers from multiple lenders and compare costs and terms with other types of financing. Look for any benefits, such as rate discounts, a lender might provide for enrolling in autopay. Also, keep an eye out for disadvantages, including minimum loan amounts or expensive late payment fees.

3. Gather your loan documents

Be prepared to verify your income and financial information with documentation. This includes pay stubs, W-2s (or 1099s if you’re self-employed), and bank statements, to name a few.

4. Complete the loan application process

Depending on the lender you choose, you may have a fully online loan application, one that is conducted via phone and email, or even one that is conducted in person at a local branch. In some cases, your mortgage application could be a mix of these options. Your lender will review your application and likely order a home appraisal, depending on the type of home improvement loan. You’ll get approved and receive funding if your finances are in good shape.

Get started on your home improvement loan. Start here

FAQ: Home improvement loans

Check home improvement loan options and rates. Start hereYou can use the money from home improvement loans for any purpose you like—even putting the cash into your checking account and savings account. However, it’s best to apply the funds towards home renovations, such as a kitchen remodel or fixing a leaky roof.

The best loan for home improvements depends on your finances. If you have accumulated a lot of equity in your home, a HELOC, or home equity loan, might be suitable. Or, you might use a cash-out refinance for home improvements if you can also lower your interest rate or shorten the current loan term. Those without equity or refinance options might use a personal loan or credit cards to fund home improvements instead.

That depends. We’d recommend looking at your options for a refinance or home equity-based loan before using a personal loan for home improvements. That’s because interest rates on personal loans are often much higher. But if you don’t have a lot of equity to borrow from, using a personal loan for home improvements might be the right move.

The credit score requirements for a home improvement loan depend on the loan type. With an FHA 203(k) rehab loan, you likely need a good credit score of 620 or higher. Cash-out refinancing typically requires at least 620. If you use a HELOC, or home equity loan, for home improvements, you’ll need a FICO score of 680–700 or higher. For a personal loan or credit card, aim for a score in the low-to-mid 700s. These have higher interest rates than home improvement loans, but a stronger credit profile will help lower your rate.

If you’re buying a fixer-upper or renovating an older home, the best renovation loan might be the FHA 203(k) mortgage. The 203(k) rehab loan lets you finance (or refinance) the home and renovation costs into a single loan, so you avoid paying double closing costs and interest rates. If your home is newer or of higher value, the best renovation loan is often a cash-out refinance. This lets you tap the equity in your current home and refinance into a lower mortgage rate at the same time.

Home improvement loans are generally not tax-deductible. However, if you finance your home improvement using a refinance or home equity loan, some of the costs might be tax-deductible.

Disclaimer: The Mortgage Reports do not provide tax advice. Be sure to consult a tax professional if you have any questions about your taxes.

Discover the best home improvement loans for your project

Embarking on a home renovation journey? Discover the best loan for home improvement by comparing quotes from multiple lenders.

Whether you’re looking into home remodel loans, renovation loan options, or simply need home improvement financing, we’ve got you covered.

Click the link below to explore home renovation lenders and find the ideal home improvement loan to turn your house into the home of your dreams.

Time to make a move? Let us find the right mortgage for you