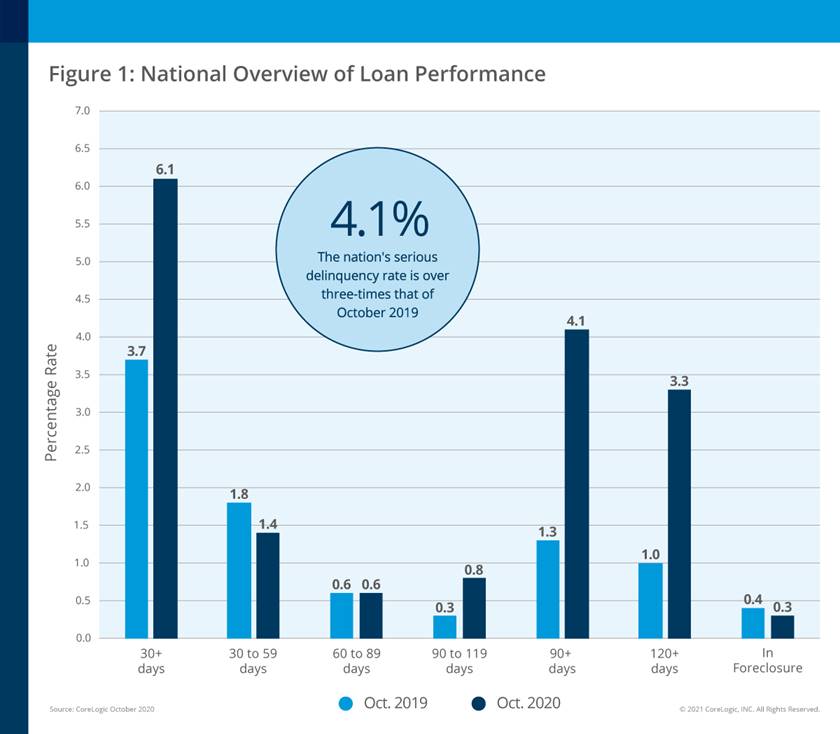

CoreLogic® recently released its monthly Loan Performance Insights Report for October 2020. On a national level, 6.1 percent of mortgages were in some stage of delinquency (30 days or more past due, including those in foreclosure). This represents a 2.4-percentage point increase in the overall delinquency rate compared to October 2019, when it was 3.7 percent. Notably, serious delinquency is over three times that of October 2019, but down from the previous two months.

To gain an accurate view of the mortgage market and loan performance health, CoreLogic examines all stages of delinquency, including the share that transitions from current to 30 days past due. In October 2020, the U.S. delinquency and transition rates, and their year-over-year changes, were as follows:

Early-Stage Delinquencies (30 to 59 days past due): 1.4 percent, down from 1.8 percent in October 2019.

Adverse Delinquency (60 to 89 days past due): 0.6 percent, unchanged from 0.6 percent in October 2019.

Serious Delinquency (90 days or more past due, including loans in foreclosure): 4.1 percent, up from 1.3 percent in October 2019, but down slightly from 4.2 percent in September and 4.3 percent in August.

Foreclosure Inventory Rate (the share of mortgages in some stage of the foreclosure process): 0.3 percent, down from 0.4 percent in October 2019. The foreclosure rate has stayed at 0.3 percent for seven consecutive months, which was the lowest since at least January 1999.

Transition Rate (the share of mortgages that transitioned from current to 30 days past due): 0.8 percent, up from 0.7 percent in October 2019.

Job loss and increased closures of small businesses triggered higher delinquency rates during the pandemic. A record amount of home equity, and the CARES Act loan forbearance, have helped to keep borrowers out of foreclosure, leading to a decline in the foreclosure rate despite high delinquency rates.

“After a financially challenging year, the healthy housing market and new stimulus measures are helping borrowers get back on their feet,” said Frank Martell, president and CEO of CoreLogic. “Given these variables, we should begin to see a reduced flow of homes in delinquency in the coming months.”

“During early autumn, the improving economy enabled more families to remain current on their home loan,” said Dr. Frank Nothaft, chief economist at CoreLogic. “In September and October, 0.8 percent of current borrowers transitioned into 30-day delinquency. This is the same as the monthly average for the 12 months prior to the pandemic, and well below the record peak of 3.4 percent of borrowers transitioning into delinquency that we observed in April 2020.”

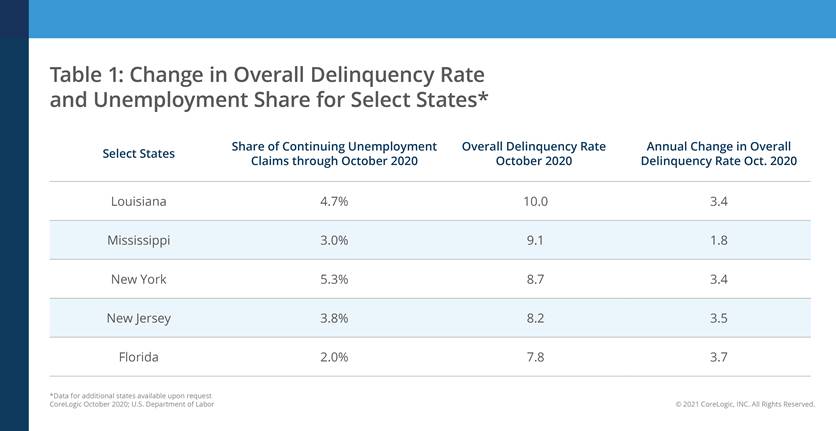

In October, every state logged an annual increase in overall delinquency rates, with Hawaii (up 4.7 percentage points) and Nevada (up 4.6 percentage points) again topping the list for gains in October. Hawaii began lifting travel restrictions in mid-October, so we may see the growth of tourism reverse some of the economic effects of the pandemic.

Similarly, nearly all U.S. metro areas logged an increase in overall delinquency rates in October. Lake Charles, La.—which was severely impacted by Hurricane Laura in August—experienced the largest annual increase for the second consecutive month with 11 percentage points. Other metro areas with significant overall delinquency increases included Odessa, Texas (up 10.3 percentage points); Kahului, Hawaii (up 7.8 percentage points) and Midland, Texas (up 7.5 percentage points).

For more information, please visit www.corelogic.com.